Volume Analysis | Flash Update – 4.21.25

The Curious Case of the VW Formation

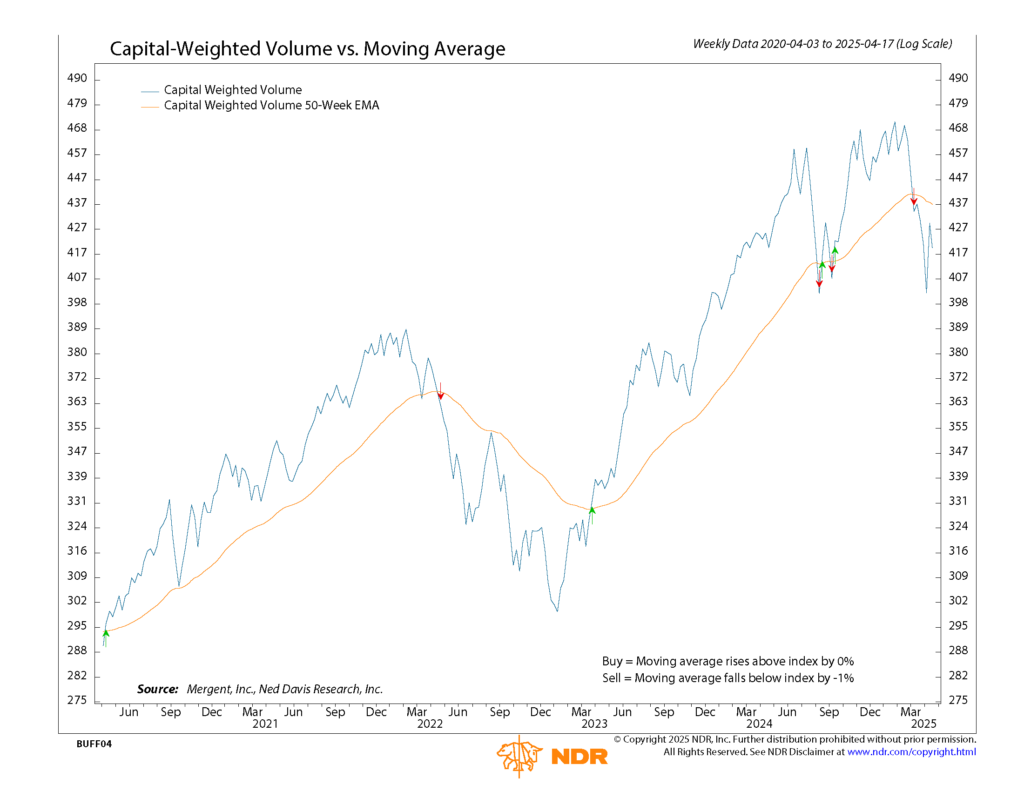

In early March, the market’s defenses began to falter. On March 7th, our capital-weighted volume metric broke ranks, breaching both structural support and our critical 1% threshold, signaling a Volume Analysis correction. Later, with the threat level elevated, on March 21st, capital-weighted dollar volume followed suit, confirming a double-barreled violation across our proprietary systems. The result: a Volume Analysis Bear Market.

But even in the fog of war, new patterns emerge. On April 11th, I SPY’d, with my little eye, a VPCI VW Bottom, and our capitulation-based re-entry signal was activated: the VPCI V bottom. Yet this wasn’t just any ordinary V-bottom. No, this signal bore markings of something far rarer.

We’ve long tracked the elusive VPCI V bottoms, and while each formation tells its own story, this one reads more like a classified case file than a common occurrence. Rarer still is the VPCI W bottom — essentially two miniature V-bottoms in sequence. In these, the selling lacks the full severity of a deep V (sub -4), but a W bottom only demands two mild triggers (under -0.4) within a month’s span. If you received our report for awhile now, you might remember September 30th, 2022, was our most recent VPCI W bottom. Both V & W VPCI bottoms require the S&P 500 to be at least 10% below its recent high.

This recent April 11th trigger isn’t just a V or a W. It’s both. A VW bottom — a hybrid formation I can’t recall seeing even during the battlegrounds of October 2008. It meets every criterion, including the 10% decline in the S&P 500 Total Return Index from recent highs (March 11th’s VPCI V bottom failed to measure up on a close-to-close basis). Perhaps most fascinating of all, however, is its timing. This VPCI signal was fired after the market’s rebound had already begun — nearly 11% off the lows when the trigger fired. Most V-bottoms strike as markets bottom out. This one arrived fashionably late. I am curious to see how this VW will play out.

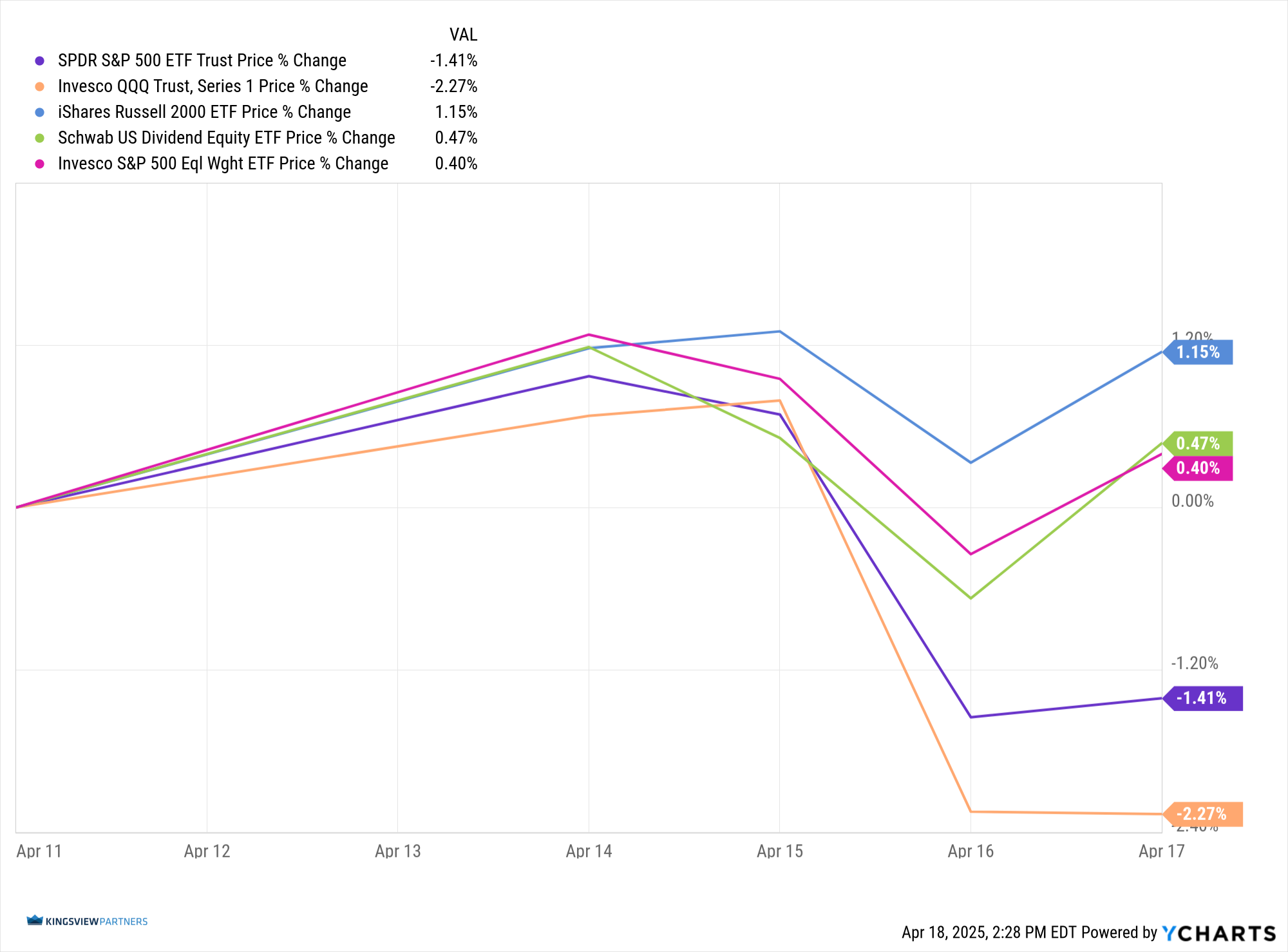

On the tactical front, despite the week’s Good Friday-shortened week, volume firepower leaned heavily toward the downside — nearly 70% of capital-weighted volume. Yet not all regiments retreated. The NYSE advance–decline line gained ground, rising on the week. Our troops, iShares Russell 2000 ETF (IWM), pushed forward 1.15%. Our brass commanders — the Schwab US Dividend Equity ETF (SCHD) and Invesco S&P 500 Equal Weight ETF (RSP) – both advanced modestly (+0.47% and +0.40%, respectively). But our generals, the tech-heavy Invesco QQQ Trust (QQQ), retreated -2.27%, while its SPYing lieutenant, SPDR S&P 500 ETF (SPY), slipped -1.41%, a casualty of market rotation.

In the backdrop, a new ghost has stirred — The Lutey Rule has sounded its alarm. Part economic intelligence, part technical recon, this rule is designed to detect recessionary risk through prolonged yield curve inversions matched with stock market declines. Although I am not an economist (minored in college), it is notable that the recession clock is now ticking according to the Lutey Rule recession indicator. The Lutey Rule is designed to sniff out recessions and their duration. I like it because it synergistically combines macroeconomics with technical analysis’s discounting mechanism. The Lutey Rule recession setup involves a prolonged inversion of the yield curve, and its differentiated trigger is an amended death cross on the S&P 500 (21-day MA crosses under 200-day MA). There are more nuances I am not covering, but historically, the Lutey Rule’s signals and duration indications have lined up well with St. Louis Fed recessions. If you are interested in learning more about the Lutey Rule, you can read up on Dr. Lutey’s paper (International Journal of Accounting and Finance ) Lutey and Rayome (2020) or DrLutey recession Indicator.

As in Agatha Christie’s tale, clues are scattered — each signal a piece of a larger mystery. But while others may wait until the final chapter, we prefer to follow the data’s trail before the lights go out.

Final orders: Active risk management may not always align with the crowd, but it remains one of our most disciplined and strategic weapons in the field.

Grace and peace my friends,

BUFF DORMEIER, CMT

Updated: 4/21/2025. Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. Investment advisory services offered through Kingsview Wealth Management, LLC (“KWM”), an SEC Registered Investment Adviser.