Volume Analysis | Flash Update – 6.1.26

Ceasefire Rally, Capital Retreat

Oil sank and stocks surged as discussions of an extended ceasefire in Iran raised hopes that the fog of war may begin to lift. On the surface, the equity battlefield responded with relief. Most of our units gapped higher on the week and closed at all-time weekly highs. Yet beneath the price advance, liquidity and capital flows told a less celebratory story. The rally marched forward, but the supply lines were not fully committed.

All major formations advanced except the dividend brass commanders, represented by the Schwab U.S. Dividend Equity ETF, which failed to join the broader charge. The rest of the field showed strength in price, but the internal flow data suggested quiet distribution to the rally rather than full institutional reinforcement.

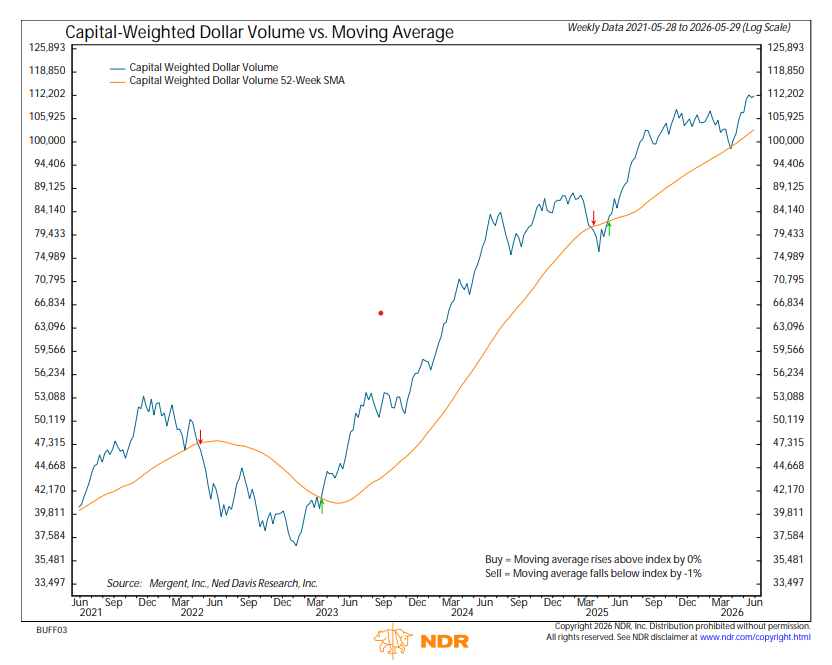

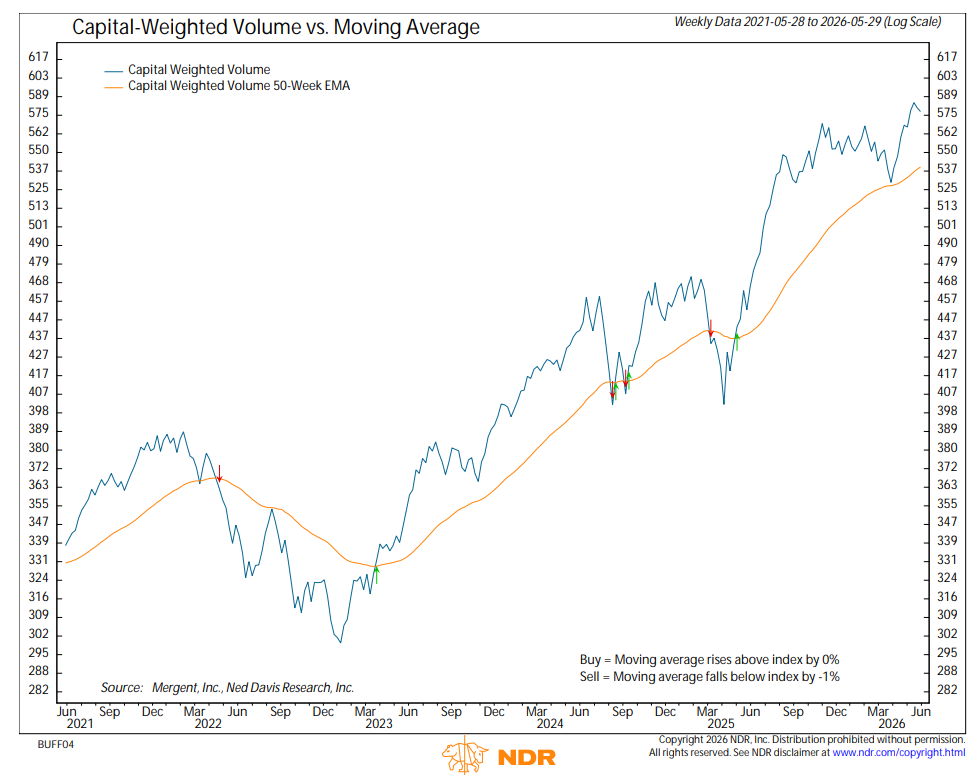

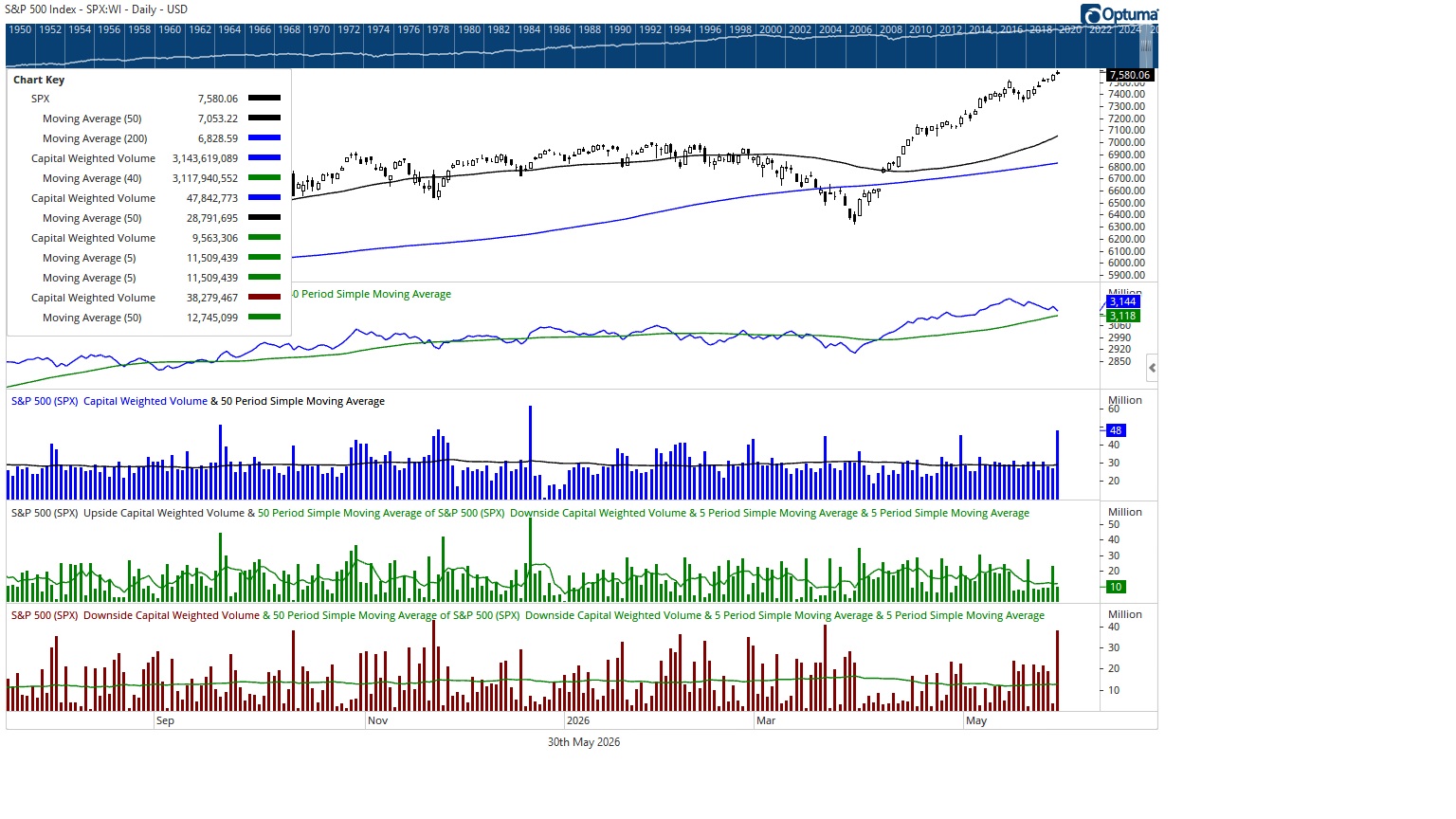

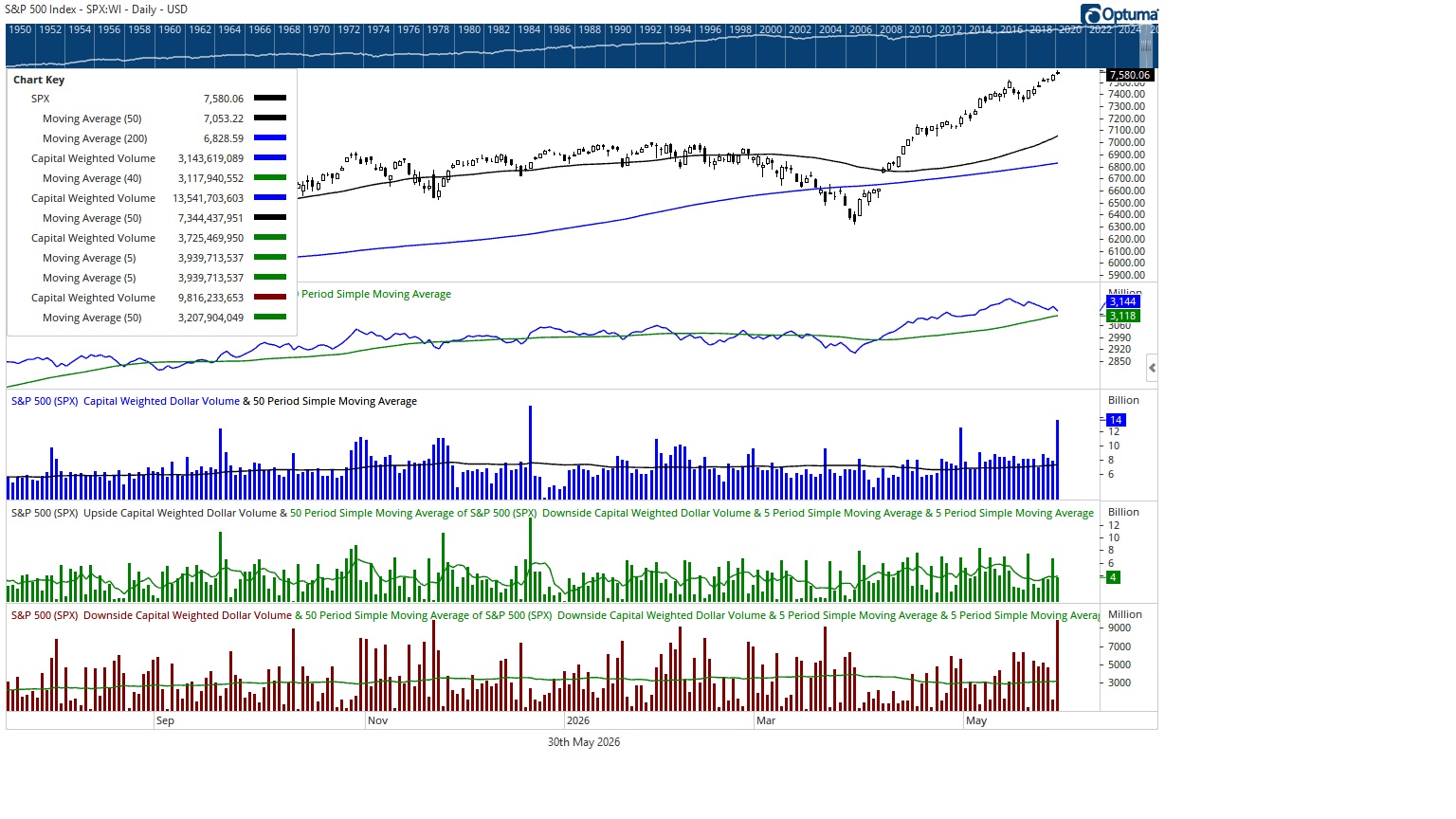

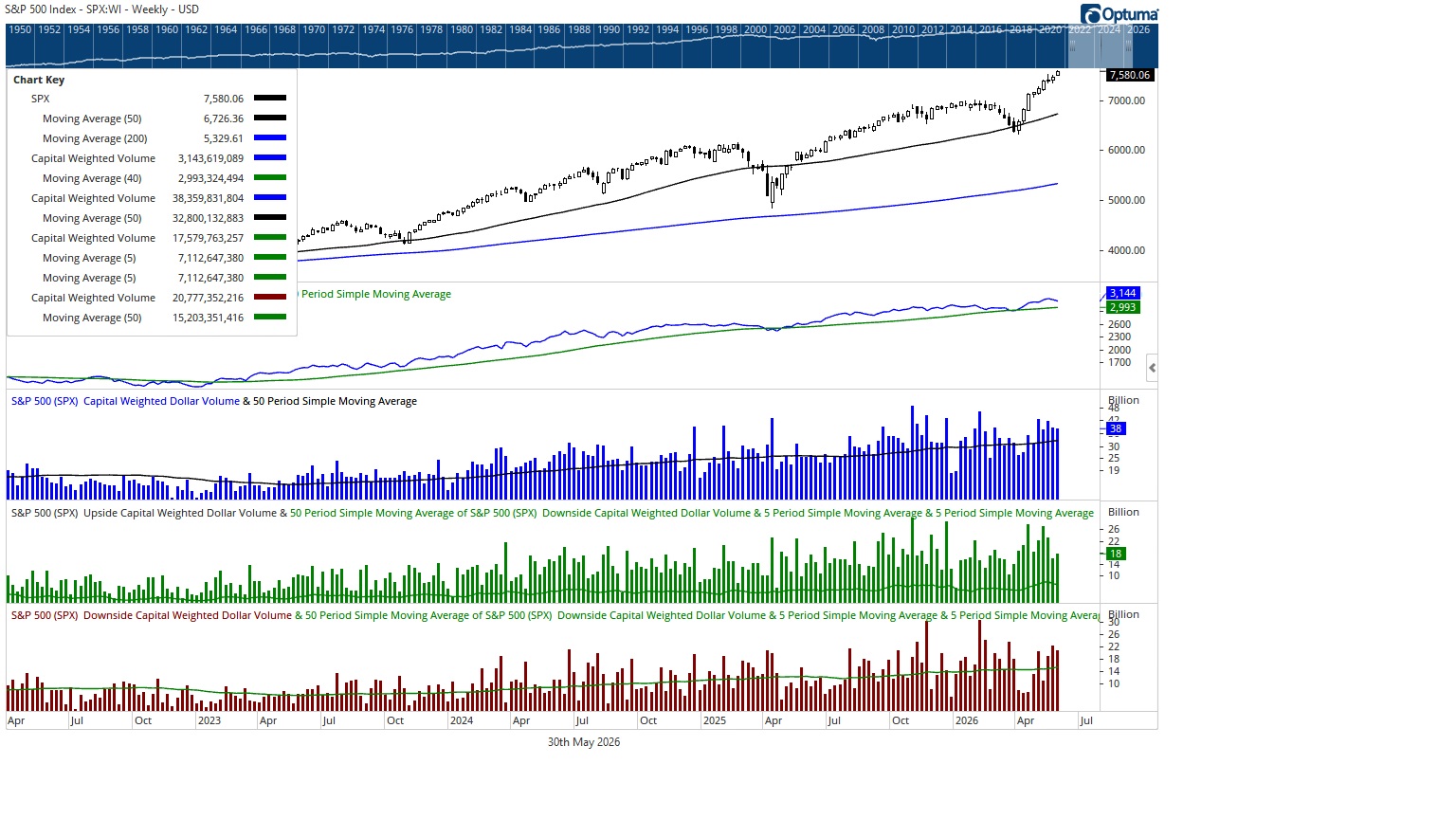

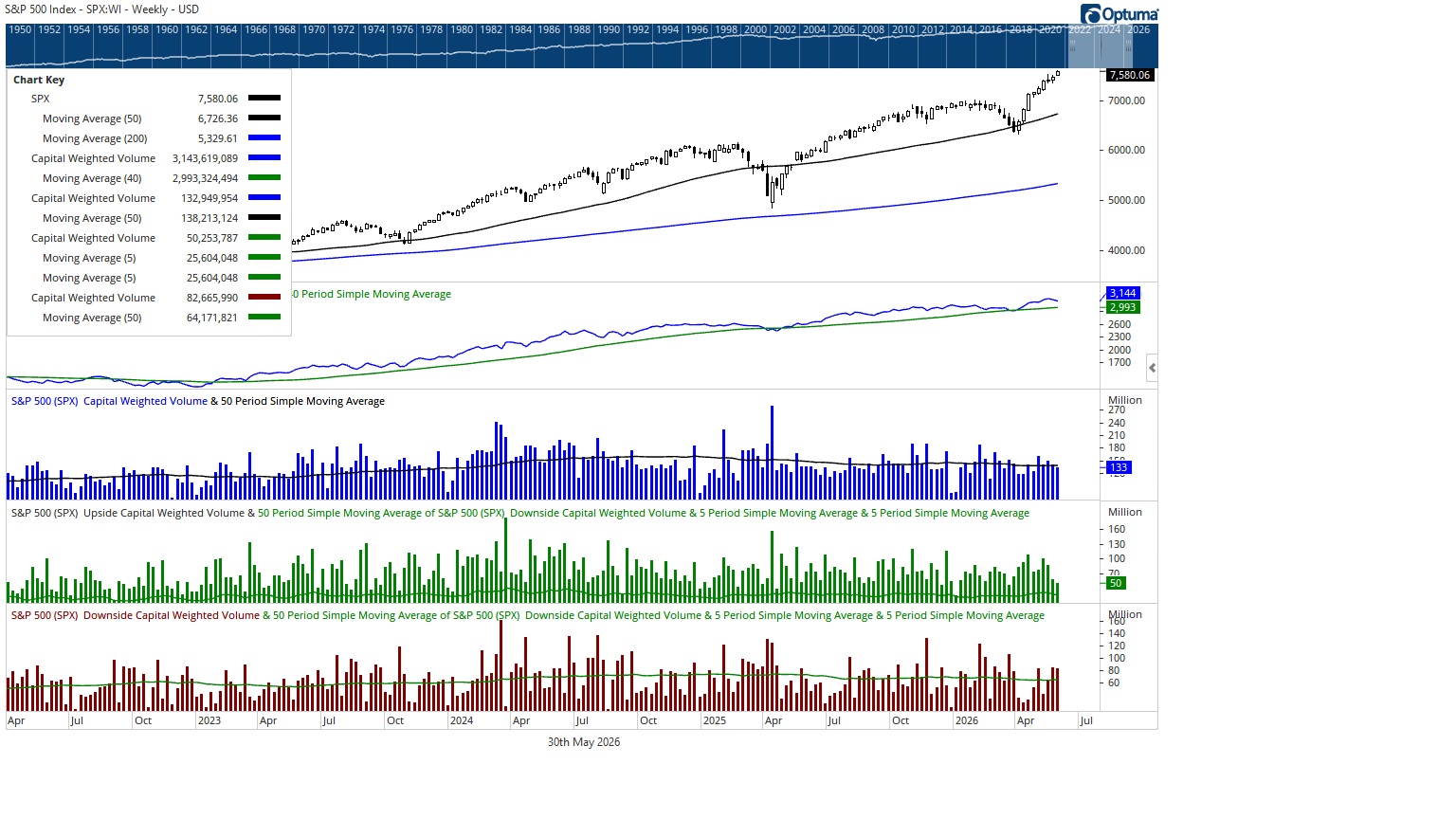

For the week, Capital Weighted Dollar Volume was high, yet 54% of capital flows were outflows. Inflows were average, while outflows ran above average. Weekly Capital Weighted Volume was slightly below average, with upside volume below average and downside volume above average, with over70% of the volume to the downside. In other words, price advanced, but capital was marching in a different direction.

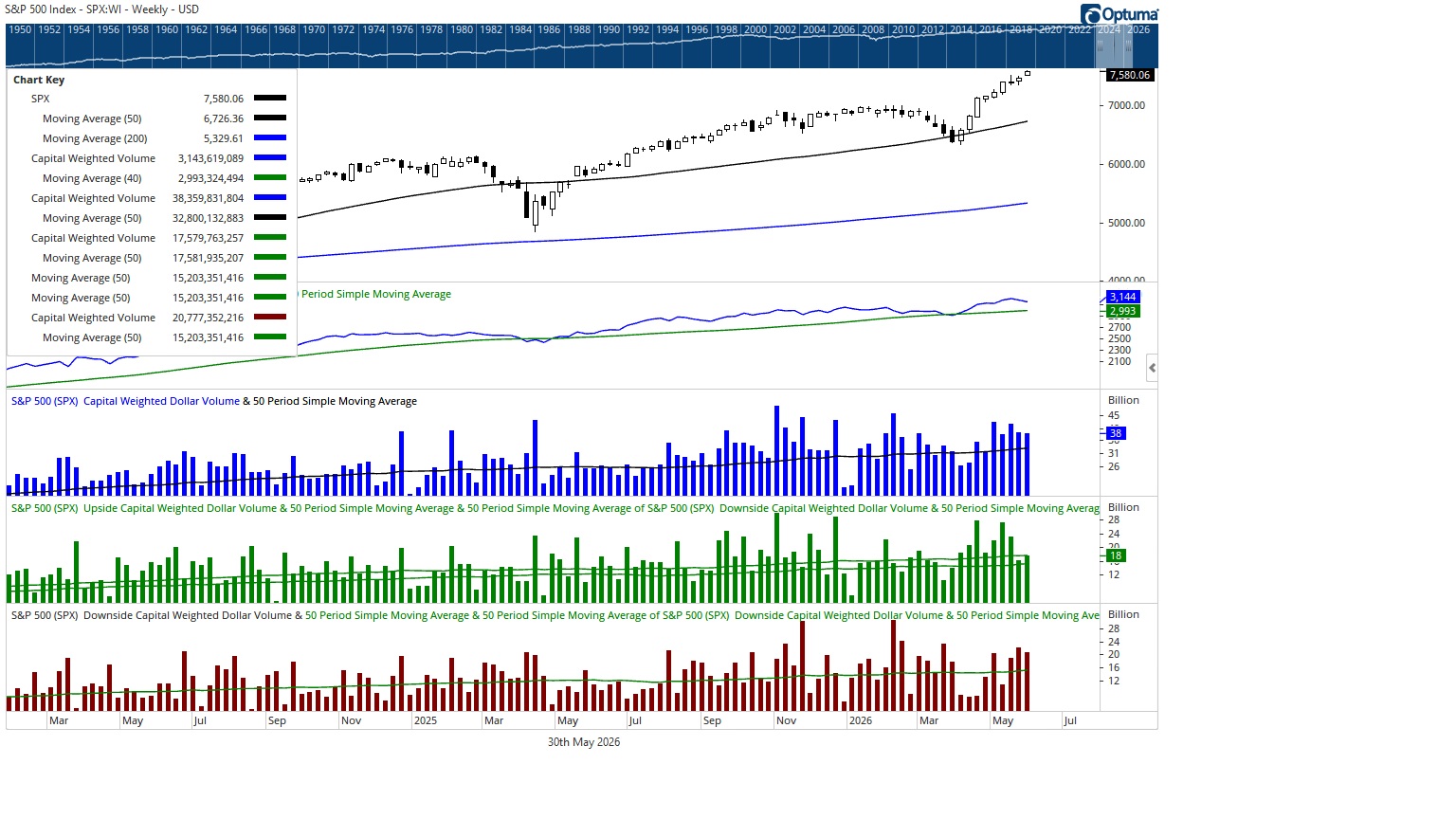

The S&P 500 closed the week on an ominous note despite finishing Friday slightly higher. Friday, March 29th, recorded the highest S&P 500 capital flow day since November 25th and the highest total Capital Weighted Volume since December 19th, 2025. Yet 73% of Friday’s capital flows were outflows, even as the S&P 500 price index closed modestly higher. Capital Weighted Volume also registered its highest daily reading since December 19th, with the largest downside print since March 20th, with more than 80% of daily volume to the downside. That is not a small warning shot. It is the kind of battlefield report that says the advance may be moving forward while heavy artillery fires from behind the ridge.

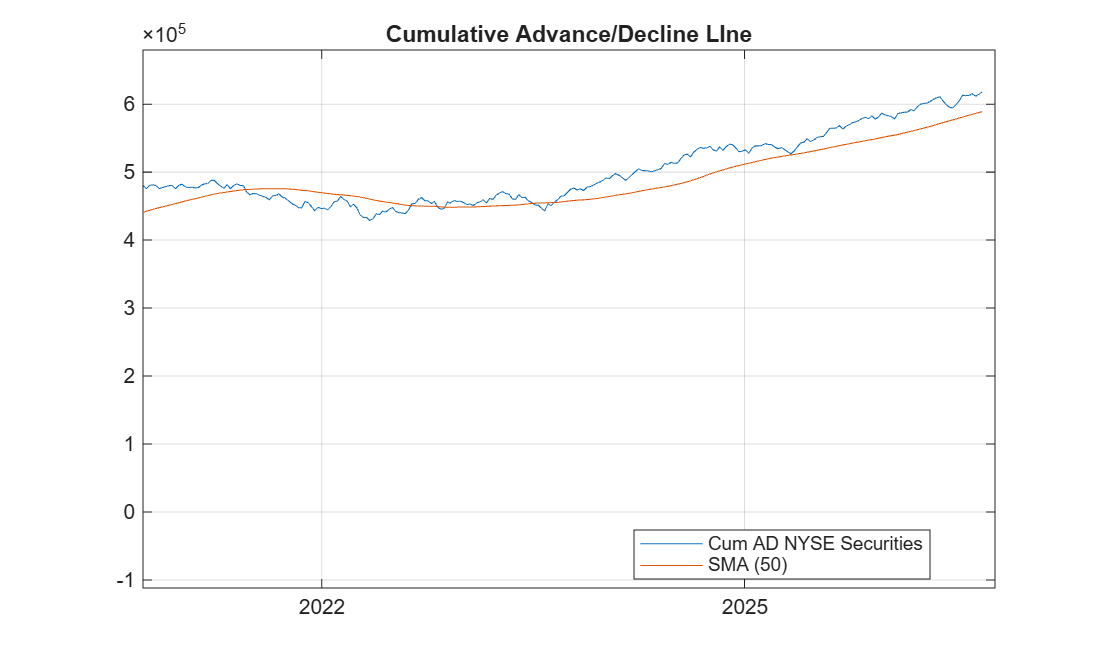

Market breadth also offered a mixed signal. The NYSE Advance Decline Line gapped higher and closed up on the week, but it finished near its weekly low, above trend yet still below prior all-time highs. Meanwhile, the NYSE operating companies’ only Advance Decline Line continued to press to new all-time highs. This divergence suggests that interest-sensitive issues may be dragging on the broader all issues Advance/Decline Line, while stocks continue to show healthier participation.

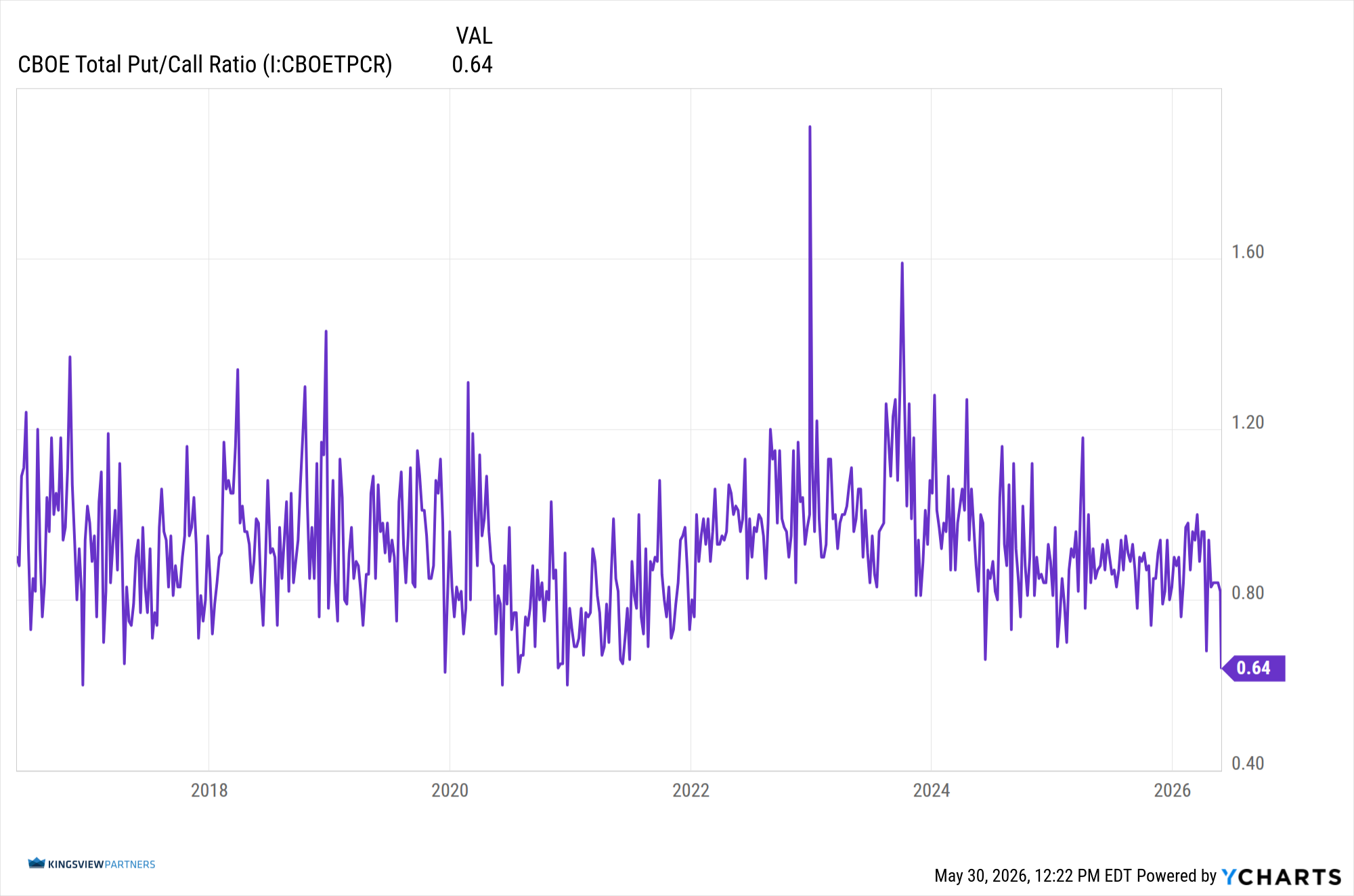

Sentiment has also shifted meaningfully. At the end of March, the CBOE Total Put Call Ratio reflected elevated pessimism. By the end of May, that same measure had fallen to its lowest weekly close since December 20th, 2020, signaling a strong appetite for risk. The troops are no longer fearful. If anything, they may be growing too confident.

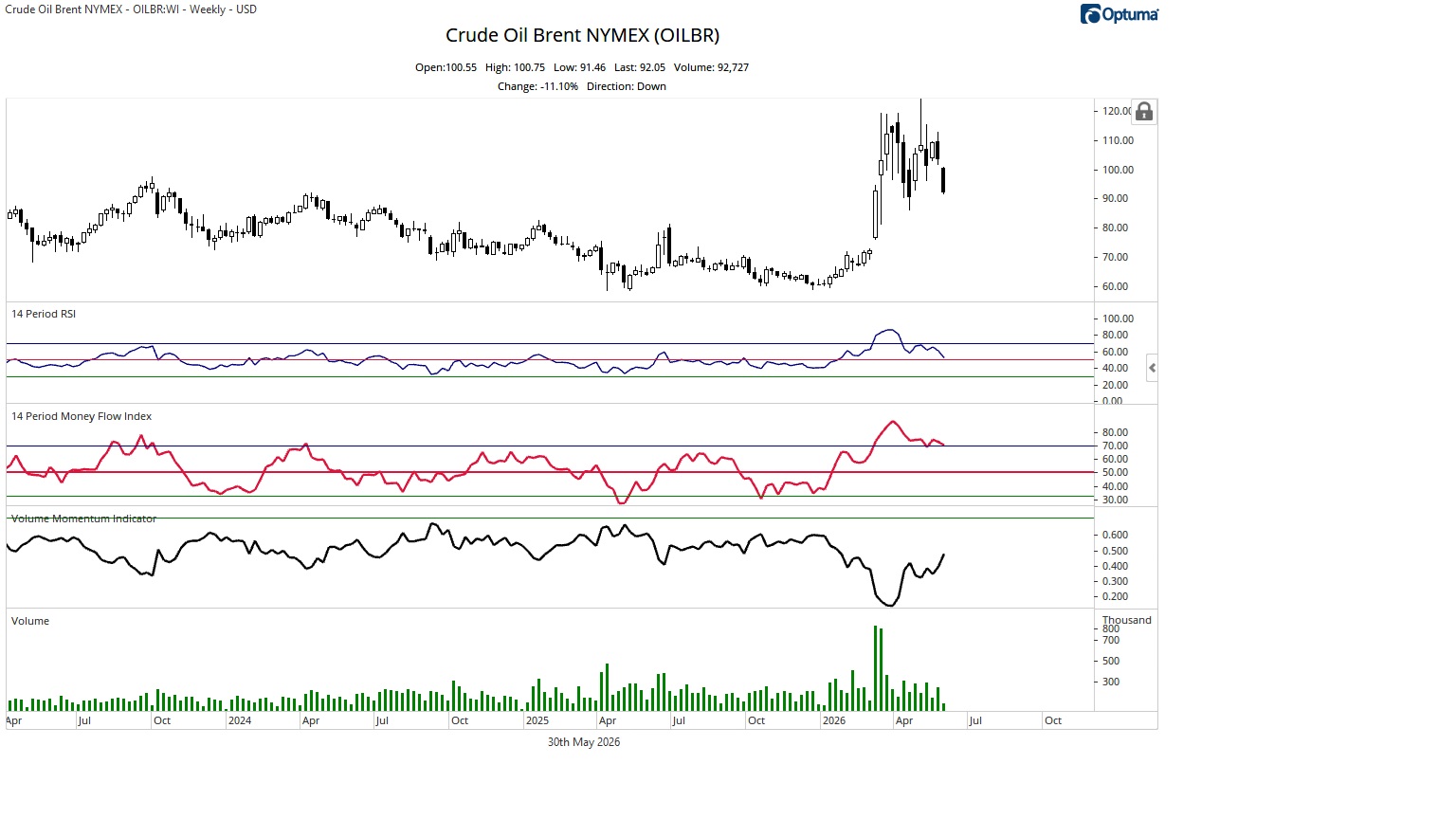

On the commodity front, oil fell nearly 7% on the week while remaining inside the massive range established on March 13th. Trading volume was exceptionally light, the lowest weekly reading since the outbreak of the war. Oil price momentum has weakened significantly, yet money flow remains bullishly extended. This suggests the energy front has lost tactical ground, but not necessarily strategic sponsorship. The ceasefire narrative may have cooled the oil advance, but the March battlefield range still defines the campaign.

Gold and silver closed modestly lower but mostly flat on the week, trading near support. Precious metals did not sound a decisive warning, nor did they confirm a full retreat from defensive positioning. The commodity scouts remain active, but no clear shofar has sounded from that front.

In the spirit of And Then There Were None, the list of concerns is narrowing in some areas but widening in others. Price has broken higher. Operating company breadth remains constructive. Sentiment has flipped to bullish, which is typically interpreted as bearish. Capital flows show distribution, downside volume is rising, and the broader Advance Decline Line has not confirmed the strength seen in price.

The bulls have taken more ground, but the field report is not clean. This was not a rout of the bears. It may be a FOMO relief rally fueled by ceasefire hopes, while larger capital quietly reduced exposure into strength.

Risk Command

This remains a market that deserves respect, but not blind trust. Price is strong, but capital flows are now beginning to show signs of being conflicted. Breadth is constructive in operating companies, but less convincing across the broader field. Sentiment has shifted from fear toward confidence, which may support rallies but also leaves less room for surprise.

Investors should remain disciplined. Position sizing, diversification, and attention to capital flow confirmation remain essential. If price strength is joined by improving inflows and stronger breadth confirmation, the campaign can continue. If outflows persist while price advances, the rally could be vulnerable to reversal.

For now, the bulls hold the field, but the supply lines are under inspection. In war and in markets, victory is not declared by movement alone. It is confirmed by the capital willing to defend the ground.

Grace and peace,

BUFF DORMEIER, CMT

Updated: 6/1/2026. Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. Investment advisory services offered through Kingsview Wealth Management, LLC (“KWM”), an SEC Registered Investment Adviser.