Portfolio Manager Insights | How Residential and Commercial Real Estate Impacts Markets – 3.27.2024

With major stock market indices hovering around all-time highs, some investors continue to worry about the state of the economy. While trends around inflation and jobs have been positive, putting the Fed in a position to cut rates later this year, there are still many concerns in areas such as real estate. This is because real estate is not just another asset class but a large sector of the economy that impacts consumer net worth, inflation, financial stability and more. What do long-term investors need to know about stresses in the real estate market?

Perhaps more than any other sector, real estate has borne the brunt of higher interest rates over the past few years. Recent developments in both residential and commercial real estate have only added to uncertainty in these markets. In residential real estate, the recent National Association of Realtors (NAR) settlement upends decades of established pricing for agents. Specifically, plaintiffs argued that the typical 5 or 6% commission that is split between the buyer’s and seller’s agents is anti-competitive. While the effects of the NAR settlement will take time to materialize, it potentially opens the door for new business models and more competitive fees.

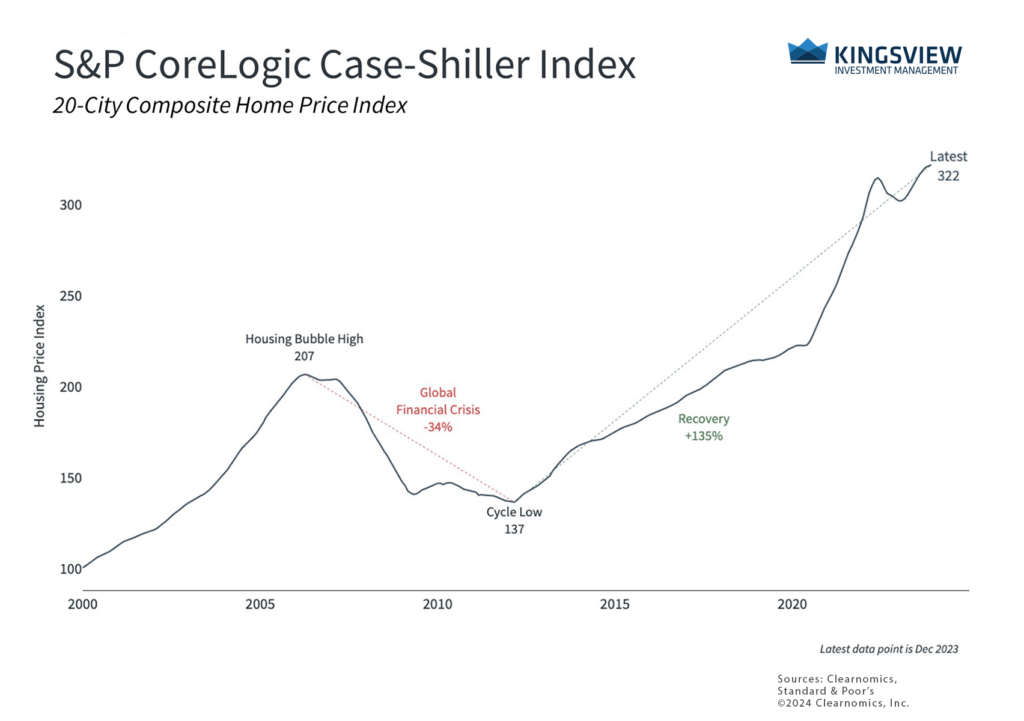

Housing prices are at record levels

At the risk of oversimplifying, economic theory suggests that in any industry, monopoly pricing restricts activity. At a more competitive price, there is likely to be more demand which in this case would be for agents’ services by real estate buyers and sellers. At the margin, this would then translate into more transactions since the overall costs would be lower. In economics parlance, the net result is that some “producer surplus” shifts to consumers, and there is less of a “deadweight loss.” In a textbook world, a more competitive market for real estate agent services is good for consumers and society since more mutually beneficial transactions occur, although the industry would also need to evolve.

This is happening at a time when home prices are back to record levels, as shown in the chart above. However, the number of transactions has remained low due to the level of interest rates and supply. Housing starts have stabilized and are beginning to creep up, and there has been a rebound in existing home sales as well. Given where prices are and the level of underlying demand, many economists hope that more flexible commissions could help to boost the housing market in the years to come.

This affects monetary policy as well. The fact that “shelter” costs make up over a third of the Consumer Price Index basket is one reason the pace of inflation improvements has slowed. While economists and the Fed have expected price pressures in rent and mortgage payments to ease, this has not yet materialized. At his most recent press conference, Fed Chair Jay Powell addressed this issue by saying “there’s a little bit of uncertainty about when [shelter price improvements] will happen but there’s real confidence that they will show up eventually over time.”

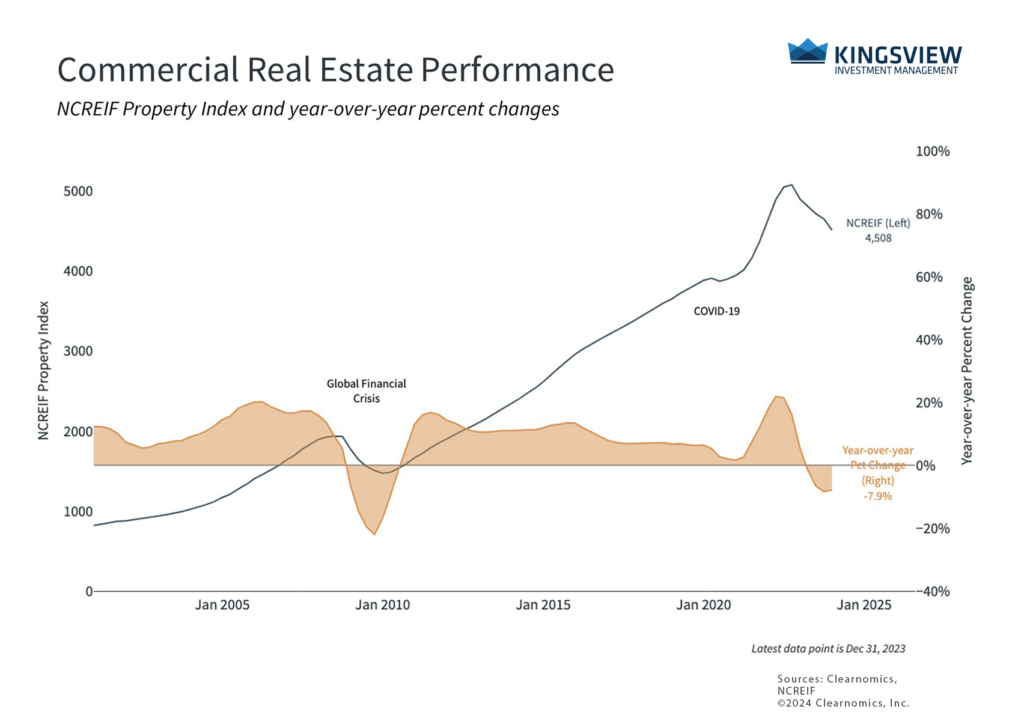

Commercial real estate prices are beginning to stabilize

In commercial real estate, recent events such the rescue of New York Community Bank (NYCB) by private investors have also raised market concerns. While the banking sector has stabilized since last year, commercial real estate has continued to struggle especially in the office and multifamily segments. Unfortunately, these areas constitute a significant portion of NYCB’s loan portfolio, much of which was acquired from Signature Bank. That acquisition also pushed NYCB’s assets above $100 billion which makes it subject to higher capital and liquidity requirements.

Thus, the issues facing NYCB can be characterized as a continuation of the problems that Signature Bank faced due to higher interest rates and a slowing economy, rather than a broader, new systemic issue. This means that it’s possible for these issues to be bank-specific rather than reflect problems across the entire financial system. One consequence of Fed rate hikes across history is the impact on banks, including the various savings and loan crises that occurred in the 1980s and 1990s. Ideally, these pressures begin to ease as the Fed loosens monetary policy in the coming months.

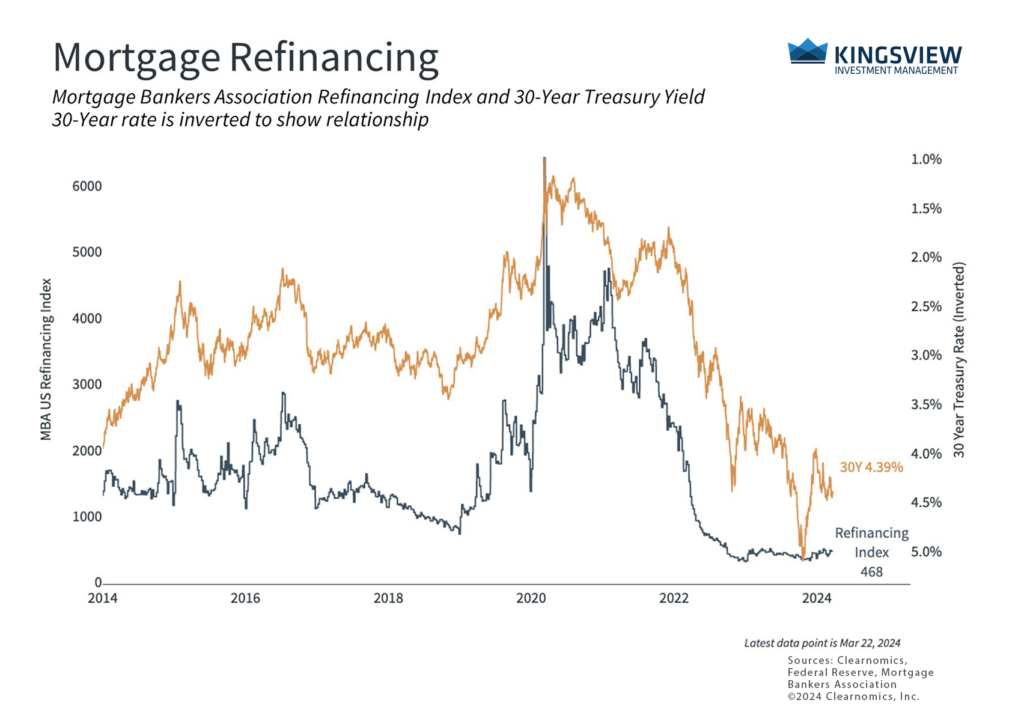

Refinancing activity has stalled due to high interest rates

Thus, there are many factors impacting all areas of the real estate market including high interest rates, the settlement on commissions, ongoing issues with CRE loans, and more. While interest rates are only one of these factors, transaction volumes should improve and financial pressures should ease as rates begin to moderate. Since the conditions that created this environment over the past few years could begin to change quickly, investors should continue to focus on the longer-term economic and market trends rather than on the rear-view mirror.

The bottom line? While there are many issues across both residential and commercial real estate, there are positive developments as well that could boost activity, especially as the Fed begins to cut rates. Investors should continue focusing on long-term trends and staying diversified.