Portfolio Manager Insights | How Investors Can Navigate Market Pullbacks, Geopolitical Risk, and More – 4.17.24

After a historically strong start to the year, markets have now pulled back 2.5% to begin the second quarter. Concerns around geopolitical tensions in the Middle East, inflation, corporate earnings, and other issues have led to a market decline, pushing the VIX index of stock market volatility to its highest level in six months. In times of market stress, it’s important for investors to maintain perspective on the critical issues and not overreact to headlines. How can investors understand and weather this period of market volatility?

First, tensions escalated in the Middle East due to an attack by Iran on Israel, the first time a direct strike has occurred between the two nations. The attack involved hundreds of drones and missiles launched from Iran and appears to have been designed to allow ample time for Israel and its allies to deploy countermeasures, resulting in minimal damage. While it’s uncertain how Israel might respond to this shot across its bow, many hope that both nations will show restraint and avoid an overt conflict.

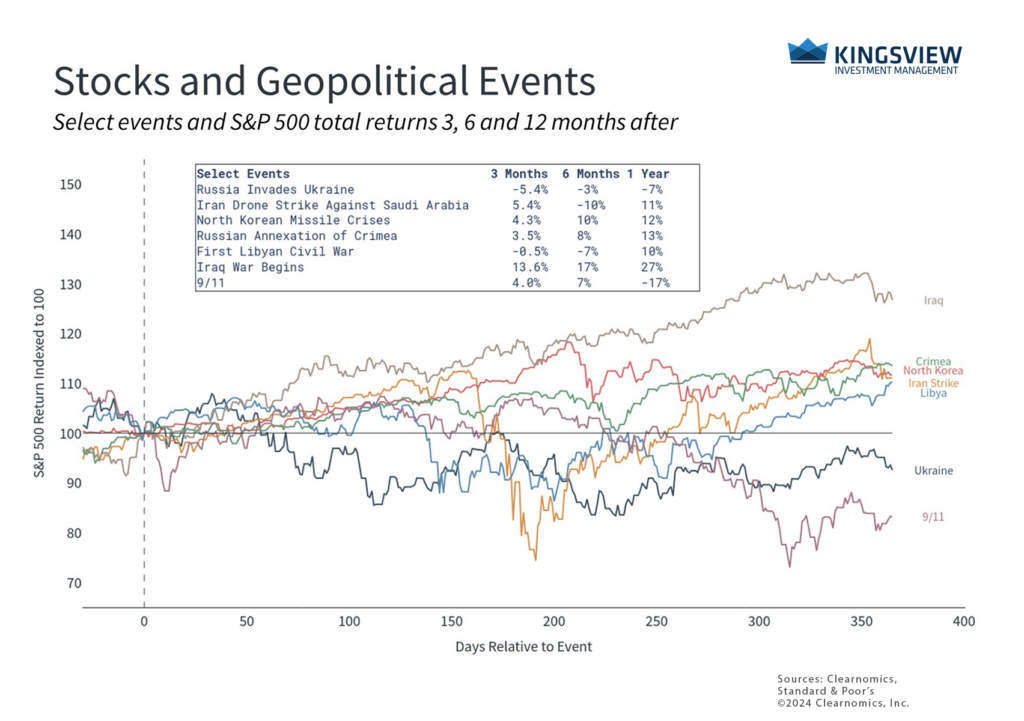

Rising geopolitical tensions add to market uncertainty

These latest developments only add to geopolitical concerns around the world. Russia’s invasion of Ukraine and the October 7 attack on Israel by Hamas only a year and a half later have already destabilized Eastern Europe and the Middle East. Without diminishing the tragic loss of life and destruction from these conflicts, investors must weigh how such events might impact the global economy, markets, and their portfolios.

Geopolitical headlines can be alarming to investors since they are unlike the typical flow of business and market news. These events are difficult to analyze and their outcomes are challenging to predict since they depend on the actions of individuals and groups with complex histories and motivations.

However, history shows that while geopolitics can impact markets, the effects are typically short-lived. The accompanying chart highlights market returns following major geopolitical events this century. Some events, such as 9/11, changed the world order and had long-lasting effects, even though it was primarily the dot-com bust that led to poor market performance. Other events, such as the war in Ukraine, resulted in higher oil prices which affected inflation and monetary policy. Most of these events did not have long-lasting effects on markets once the situation stabilized.

While today’s conflicts will be closely watched, investors ought to avoid passing judgment with their portfolios. In the long run, markets tend to recover and perform well primarily because business cycles are what matter over years and decades, despite the events that take place over weeks and months.

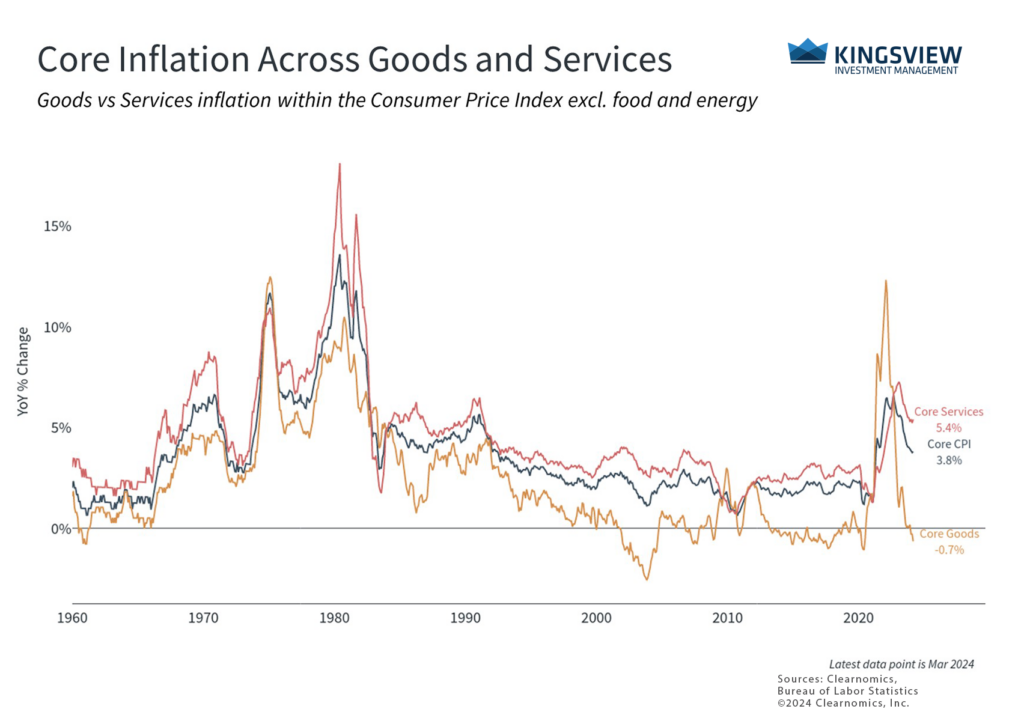

Stubborn inflation has markets rethinking the number of rate cuts

Second, many measures of inflation have proven to be more stubborn than economists had hoped. The latest Consumer Price Index (CPI) report for March showed that headline inflation remained hotter than anticipated at 3.5% year-over-year, while core inflation, which excludes food and energy prices, rose 3.8%. Rising shelter costs, i.e., the cost of renting and owning a home, are a large reason inflation has not cooled as quickly.

Combined with stronger-than-expected recent job market data, many investors now anticipate that the Fed may cut rates more slowly this year – or not at all. The Fed’s economic projections have suggested all along that it might cut rates three times this year. Market expectations, however, have swung 180 degrees since the start of the year when some believed the Fed could begin cutting rates in March or earlier. Today, markets only expect 2 or 3 rate cuts in 2024.

As always, it’s important for investors to keep these expectations in perspective. What matters for long-term investing is the direction of policy and not the exact timing or magnitude of rate cuts. There are still risks to the Fed’s outlook and the monthly inflation numbers, especially if oil prices rise further due to geopolitical conflicts. However, even if this were to occur, inflation is far more manageable today and no longer requires an emergency monetary response.

Investors should always be prepared for market volatility

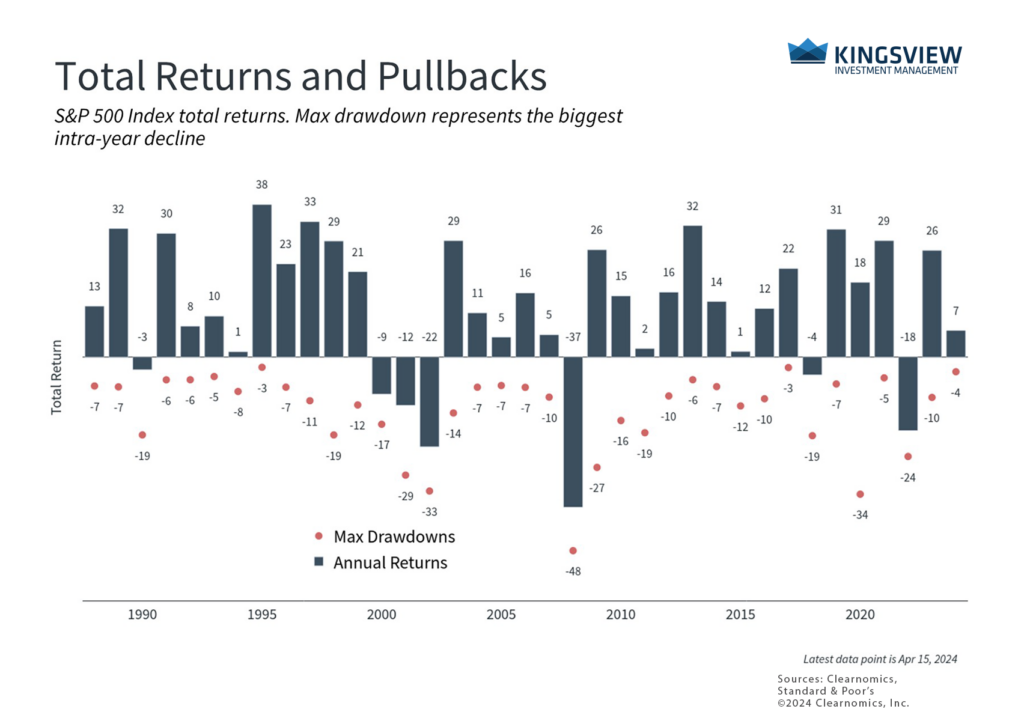

Finally, investors should keep the level of market volatility in perspective as well. While the recent 2.5% market decline is the largest since the start of the year, this follows a 10.6% total return in the first quarter. Since last October when the market began to rally, the S&P 500 has gained 28% including dividends. Since the bear market bottom in 2022, the market has gained over 50%.

The accompanying chart shows that the average year experiences significant pullbacks and that this year’s has been small by comparison. Despite these short-term challenges, markets tend to recover and often end on positive notes. This is why maintaining a diversified portfolio can help minimize short-term risk and increase the odds of financial success over time, regardless of whether markets are volatile due to the economy, the Fed, geopolitics, or other factors.

The bottom line? Markets have struggled at the start of the second quarter due to changing expectations around the Fed and escalating geopolitical tensions. Staying level-headed and keeping these events in perspective are still the best ways to achieve long-term financial goals.