Portfolio Manager Insights | What the Fed’s Hawkish Pause Means for Long-Term Investors — 6.21.23

At its June meeting, the Fed decided to hit pause on rate hikes after more than a year of rapid monetary policy tightening. Since last March, the Fed has raised rates 10 times from zero to 5%, making this the second-fastest rate hike cycle in history. However, some consider the Fed’s latest decision to be a “hawkish pause” since policymakers have penciled in two additional rate hikes later this year. With interest rates expected to remain higher for longer, what do long-term investors need to know to stay focused on their financial goals?

Perhaps the simplest way to understand the Fed’s latest move is that it is consistent with a slower pace of rate hikes, rather than a complete shift in policy. Since last December, the Fed has steadily decreased the size of each rate hike from 75 basis points (i.e., 0.75%), to 50 bps, to 25 bps, and now possibly to 25 bps every other meeting. At his latest press conference, Fed Chair Powell even inadvertently referred to the June decision as a “skip,” which implies they could raise again in July.

The Fed expects to raise rates again after skipping June

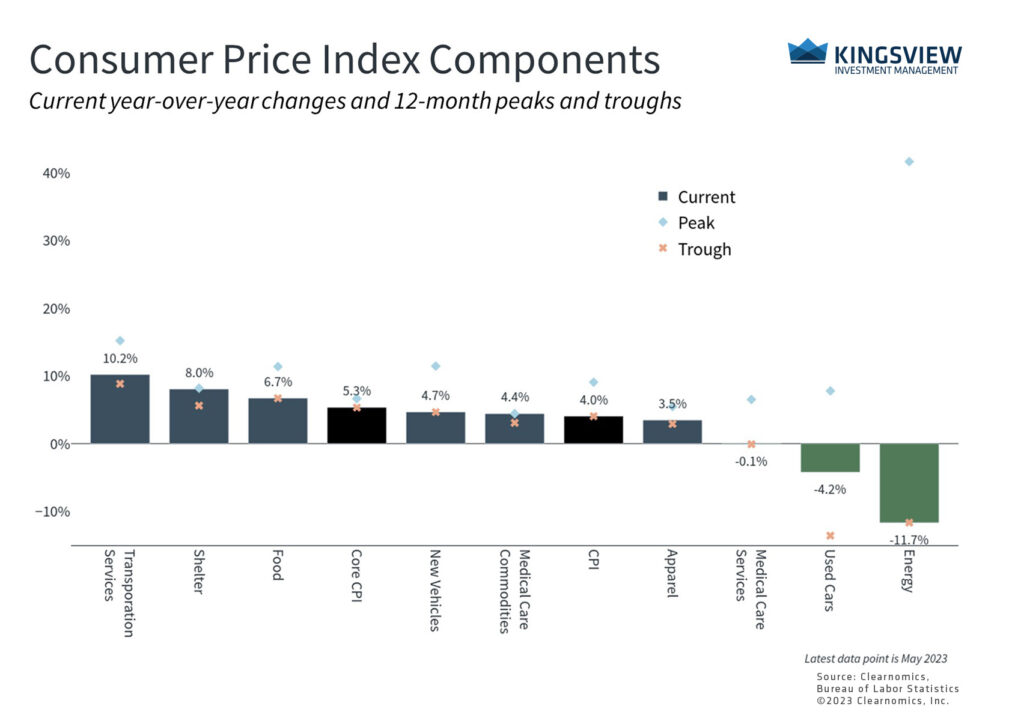

The Fed believes it is reaching a level of interest rates that is restrictive enough to slow inflation. Last week’s Consumer Price Index report, for instance, shows that overall inflation has decelerated to “only” 4% on a year-over-year basis, a significant improvement from the 9.1% pace experienced a year ago. Over this period, gasoline prices have fallen 19.7%, overall energy prices by 11.7%, and the prices of used cars and trucks have declined 4.2%. Other measures of inflation such as the Producer Price Index, also released last week, have made even more progress with the headline index rising only 1.1% year-over-year.

Why might the Fed keep rates high if inflation is already improving? The real challenge facing policymakers continues to be “core inflation,” a concept that excludes food and energy prices to better understand underlying inflation trends. From an economic perspective, inflation that is “sticky” or that threatens an inflationary spiral – i.e., when higher prices result in higher wages, which in turn result in more spending and even higher prices – is the real culprit. Since this depends on the behavior and activities of businesses and consumers, it will take time to improve.

Consumer prices are rising at a slower pace but core inflation remains a problem

For example, core inflation rose 5.3% in May compared to a year earlier – an improvement from its peak of 6.6% last September but still well above the Fed’s target. The main driver is the cost of housing, referred to as “Shelter” in the CPI report, which has increased 8% over this period and represents a third of the CPI index. Shelter consists of rent payments and what is known as “owners’ equivalent rent,” or what a homeowner would pay to rent their property. While there are signs and hopes that shelter costs will decelerate as leases are renewed, this might only slowly appear in the inflation data. Excluding shelter from core inflation, prices have risen 3.4%.

Of course, higher rates have slowed some parts of the economy, most notably in the financial and real estate sectors. Fortunately, the banking crisis that began in March appears to be stable for the time being, and has arguably benefited banks with strong balance sheets. The jump in the Fed’s own balance sheet in the aftermath of Silicon Valley Bank’s collapse, due to programs such as the Bank Term Funding Program, has already reversed. Residential real estate continues to struggle with the average 30-year fixed mortgage rate around 7%, but there are some signs that housing activity, including existing home sales, is stabilizing. Commercial real estate remains the biggest wildcard as refinancing uncertainty continues.

In contrast, many parts of the economy remain unusually strong given the level of policy rates, allowing the Fed to continue raising at a slower pace. Unemployment is still exceptionally low and the FOMC’s latest projections show that they expect it to rise to only 4.1% by year end. The stock market has also taken recent events in stride with the S&P 500 climbing 15% this year, driven largely by technology stocks. The index has risen 23% since the bottom last fall and is now only 8% below its all-time high achieved at the beginning of 2022.

Global policy rates remain high after a year of tightening

It’s worth noting that not all central banks are following the Fed’s lead. For instance, the European Central Bank decided to raise rates just a day after the Fed’s decision to pause. Unlike in the U.S. where economic growth has remained surprisingly robust and inflation has slowed, Europe is experiencing a recession after two quarters of negative growth. Eurozone inflation remains stubbornly high with the headline and core measures rising 6.1% and 6.9% year-over-year in May, respectively. Similarly, the Bank of England’s Bank Rate is currently 4.5% but markets expect a peak rate of 5.5%.

The bottom line? The Fed skipped a rate hike in June due to improving inflation but could raise rates again later this year. Either way, rates will likely remain higher for longer, especially as other central banks continue to tighten policy. The U.S. has experienced improving inflation and continued growth, fueling markets this year. Investors should continue to focus on their long-term financial goals as Fed policy evolves.

Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. Investment advisory services offered through Kingsview Wealth Management, LLC (“KWM”), an SEC Registered Investment Adviser. (2023)