Portfolio Manager Insights | How the Market Rally and Interest Rates Impact Valuations — 6.28.23

The past few years are proof that market sentiment can turn on a dime. This year’s strong market rally, with the S&P 500 rising 13% and the Nasdaq gaining 29%, has been driven by technology stocks, improving inflation, and the absence of a recession. While it may be too early to tell, some investors believe we are in the midst of a new bull market. However, with the Fed and other central banks signaling further rate hikes to return inflation to 2%, others are questioning the sustainability of this year’s rally. For long-term investors, who should be less concerned by day-to-day market swings, what matters more than what we call this market period is the level of valuations and interest rates. What are these factors signaling about achieving financial goals in the coming years?

It’s important to start by discussing why valuation measures matter to long-term investors. Simply put, valuations are the best tools that investors have to gauge the attractiveness of the stock market over years and decades. This contrasts with much shorter time frames during which global headlines, industry news, and company-specific events can dominate market movements. These concerns eventually settle and fade, leaving only traces of their impacts on asset prices, underlying fundamentals, or both. In this way, valuations are not market timing tools for making all-or-nothing investment decisions. Instead, valuation levels are an important input in determining appropriate asset allocations based on financial goals.

Valuations are no longer cheap after this year’s rally

Unlike stock prices on their own, valuations don’t just tell you how much something costs, but what you get for your money in terms of earnings, book value, cash flow, dividends, and other measures. After all, holding shares of a company means you are entitled to a portion of its profitability, so paying an appropriate price can improve the odds of future growth. Valuations are correlated with long-term portfolio returns for this reason – i.e., buying when the market is cheap can improve the chances of success, and buying when the market is relatively expensive can reduce future returns.

To a large extent, the reason this pattern exists is exactly because it is difficult to stay invested when markets fall and valuations are the most attractive. Just think about how most investors felt at the start of this year, or back in March 2020, or during 2008. When it comes down to it, staying patient is much easier said than done.

What do valuations tell us today? On the surface, broad stock market valuations are above both their recent lows and historic averages. The price-to-earnings ratio for the S&P 500 (based on next-twelve-month earnings) is 18.9x, well above the average of 15.6x since the mid-1980s. This metric only briefly fell to 15.3x during last year’s bear market crash before rebounding immediately. These numbers are highly dependent on the market and economic cycle and can therefore fluctuate over time. For example, the average over the past decade has been considerably higher at 17.6x, making it more difficult to interpret these valuation metrics.

Earnings growth has flatlined but is expected to pick up

A related question many investors may be facing is around the impact of higher interest rates on the market, since there are many ways in which rates and stocks are linked. Higher interest rates tend to slow the economy which then impacts company sales and profitability. Higher rates also reduce the value of cash flows far into the future, making highly uncertain businesses or those reliant on future growth less valuable, at least in theory.

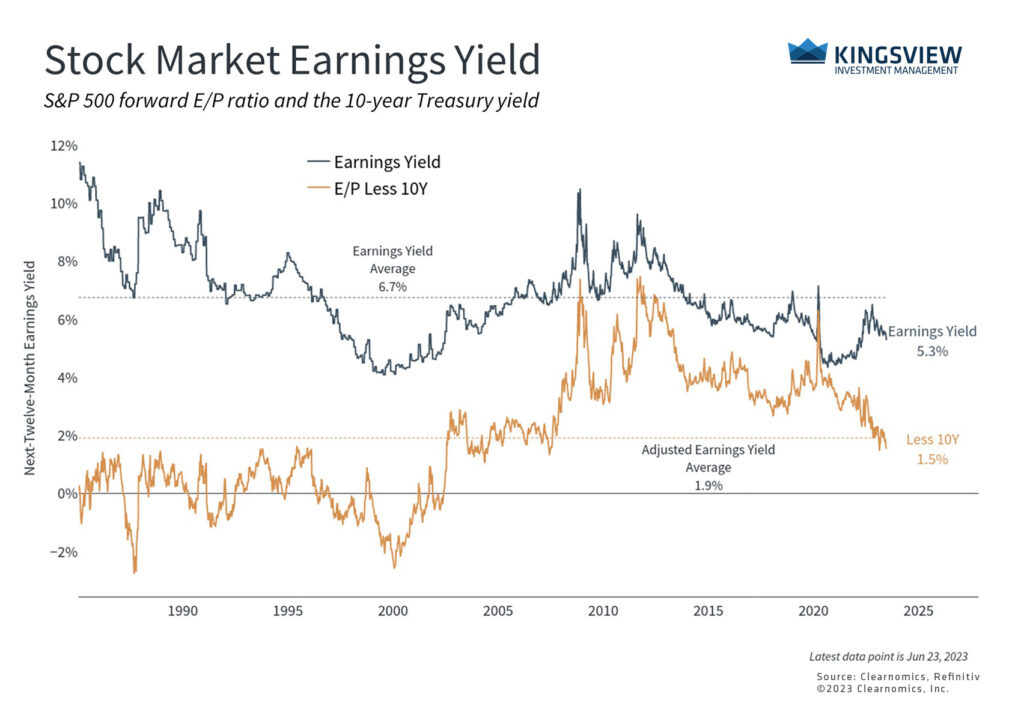

Interest rates also impact stock prices directly through financial markets and investor preferences. When rates are higher, bonds become more attractive relative to stocks since they can generate more income. The resulting headwind on stocks can be interpreted as investors shifting their portfolios toward bonds, or equivalently that stock prices should adjust so that their “yields” rise to new levels.

The first chart above highlights this relationship by focusing on the earnings yield of the S&P 500, which is just the inverse of the P/E ratio. This measure tells us how much in corporate earnings an investor is “yielding” for every dollar they invest, allowing us to think of stocks in a bond-like way. Specifically, the S&P 500 has an earnings yield of 5.3% compared to 10-year Treasury bonds yielding 3.7%. The gap between these two measures – a gauge of the relative attractiveness of stocks over bonds, has fallen as interest rates have risen. This difference is now 1.5% compared to a historical average of 1.9%. Of course, stocks are not like bonds in that earnings are not guaranteed, but this comparison is still helpful.

On the surface, these measures suggest the market is no longer cheap, which is to be expected after this year’s significant rallies. However, there are big caveats to the preceding discussion. One reason this may be harder to interpret today is that the market’s earnings yield has worsened not only because stock prices have risen, but also because earnings expectations have been flat.

However, if the economy does avoid a recession and begins to accelerate, corporate earnings could also recover. This would boost earnings yields, making stocks more attractive again. Given that even the most negative economic forecasts expect only a shallow and short-lived recession, it may be important to not focus too much on near-term earnings outlooks when interpreting valuation measures. Also, longer-term interest rates have been more stable this year despite the possibility of further Fed rate hikes. This could improve the comparison between stocks and bonds over time as well.

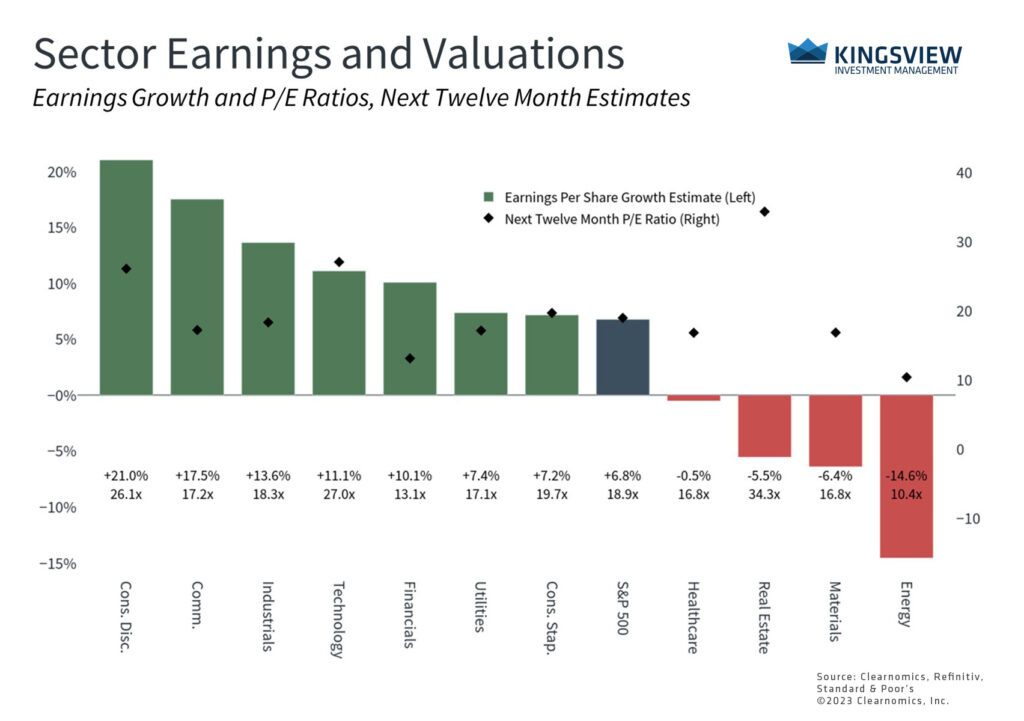

Many sectors are more attractive than the broader market

Additionally, valuations are only expensive when considering the broad market and certain sectors. Many parts of the market still look quite attractive, especially if earnings do rebound over the next year. The accompanying chart highlights both the forward-looking P/E ratios across sectors in addition to consensus earnings growth projections. It’s easy to see that there are significant differences beneath the surface of the market. Diversifying across many of these sectors, with an eye toward growth and valuations, could be increasingly important as economic uncertainty continues.

The bottom line? While valuations are not short-term market timing tools, they are among the most important metrics for constructing long run portfolios that include both stocks and bonds. This is especially true as earnings growth recovers and interest rates stabilize. Investors should focus more on valuations than day-to-day headlines in order to stay focused on their financial goals.

Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. Investment advisory services offered through Kingsview Wealth Management, LLC (“KWM”), an SEC Registered Investment Adviser. (2023)