Portfolio Manager Insights | How the Failure of First Republic Impacts the Financial System — 5.3.23

On the morning of May 1, it was announced that First Republic Bank had been taken over by the FDIC and sold to JPMorgan Chase. Eleven major banks had previously infused First Republic with $30 billion in deposits to stabilize the bank after the failures of Silicon Valley Bank, Signature Bank, and Credit Suisse. This process found new urgency over the past week when First Republic revealed that uninsured deposits at the bank fell $100 billion in the first quarter. Thus, this deal has been in the making for several days, with a few large banks bidding on First Republic’s deposits and assets. With ongoing banking turmoil creating market and economic uncertainty, how can long-term investors navigate the months ahead?

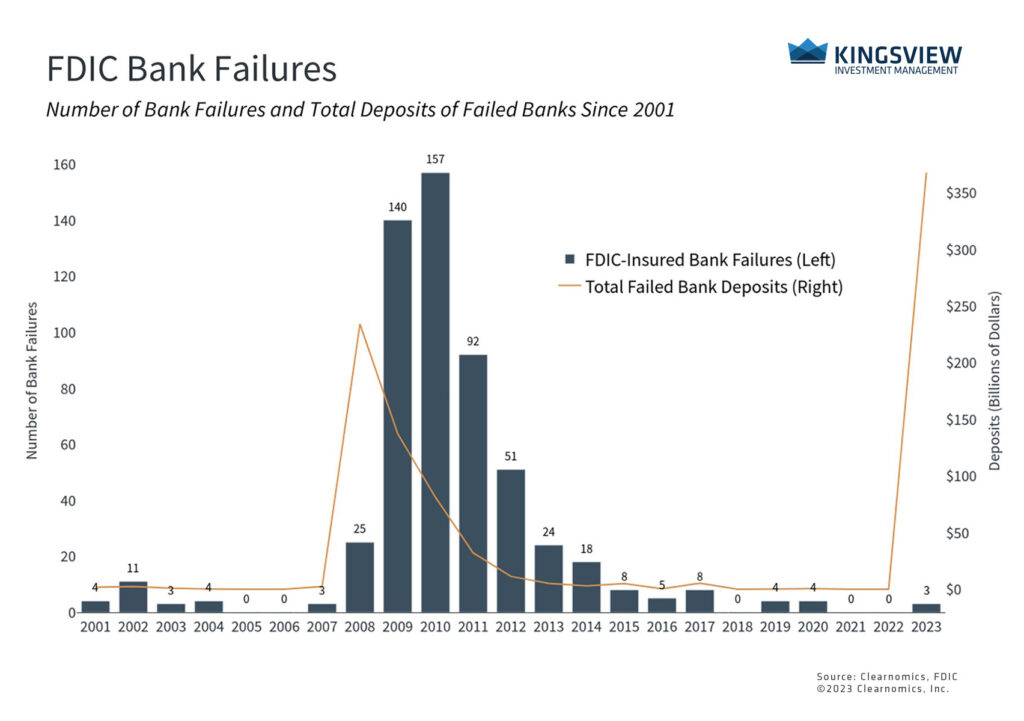

The orderly sale of First Republic is good news, but its failure mirrors the other bank failures that occurred almost two months prior. These banks grew aggressively by pursuing deposits that proved to be unstable when the economy slowed, the tech sector faltered, and cryptocurrencies plummeted. While this alone would create stress for any bank, rising interest rates also resulted in unrealized losses in their bond portfolios, which normally don’t need to be marked-to-market if they are expected to be held until maturity. However, falling deposits forced these banks to sell bonds and realize these losses.

Three FDIC-insured banks have now failed with a total of $368 billion in deposits

Thus, this banking crisis is the result of both a failure of risk management specific to these banks and the broader tightening of financial conditions due in large part to Fed rate hikes. However, banking crises are not new, and many of the biggest market shocks since the late 19th century have been due to tremors in the financial system. The Panic of 1873, for example, occurred when one of the largest banks, Jay Cooke & Company, failed due to bad bets on railroads. Others include the Panic of 1907, the 1929 crash, the Savings and Loan crises throughout the 1980s and 1990s, the 2008 global financial crisis, and many other international crises.

What all of these historical episodes have in common is the availability of money, the expansion of credit, and the eventual tightening of financial conditions. Like a sugar rush, a rapid increase in money and credit through the global financial system can drive asset bubbles and risk-taking in a particular market or across a whole country. Sooner or later, however, there is a sugar crash as returns peter out, sentiment shifts, and conditions tighten.

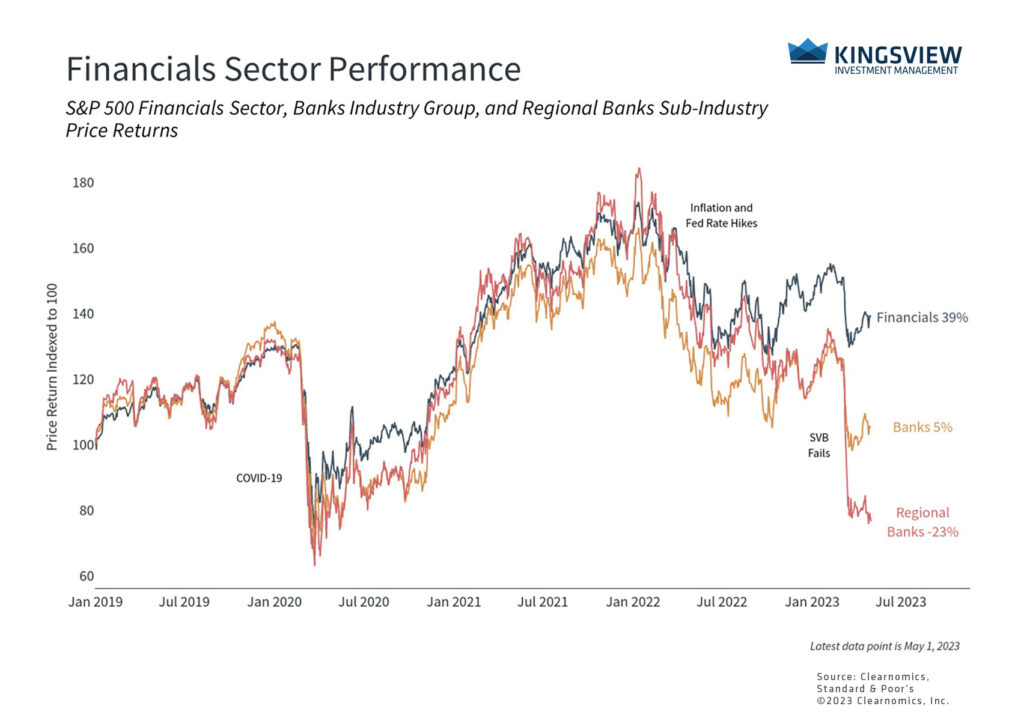

The banking crisis has been concentrated in specific regional banks

This is sometimes referred to as the “Minsky Model,” named after the 20th century economist Hyman Minsky. In short, as credit continues to expand, investors, businesses and individuals are willing to take on more and more risk. During the height of these market manias, investment returns feel easy to come by, leading to overconfidence and a fear of missing out. While this may be prudent at first, successes and gains motivate investors to take on more and more leverage until it becomes unsustainable (think the dot-com and housing bubbles). This ends when there is a “Minsky Moment” whereby some events shake investor confidence, causing it to all come crashing down. While the details naturally differ between episodes, this is what has occurred since mid-2020. More recently, this has ended with the failure of crypto companies, layoffs at large tech companies, and more.

Thus, the question today is whether there will be broader economic instability or if the situation is contained. After all, there are many surface-level parallels to 2008 which are raising investor concerns, including JPMorgan Chase’s acquisition of Bear Stearns in March 2008. As the nation’s largest bank, it’s not surprising that it would play a role in any financial crisis. The Fed had also raised rates prior to 2008 and the economy had appeared to be in good shape based on growth figures.

However, while the phrase “this time is different” can be dangerous, there are many distinctions between now and the situation fifteen years ago. Perhaps the most important is the amount of leverage in the system. The global financial crisis of 2008 wasn’t just about the housing bubble – the main issue was that banks and other institutions held significant leverage in the form of derivatives which magnified the impact of the housing market collapse. This means that even small upticks in default rates and bad loans were enough to cause large financial institutions to fail. If falling bond prices are seen as a parallel to falling home prices, there would need to be layers upon layers of leverage on these bonds to truly mirror 2008. This does not seem to be the case.

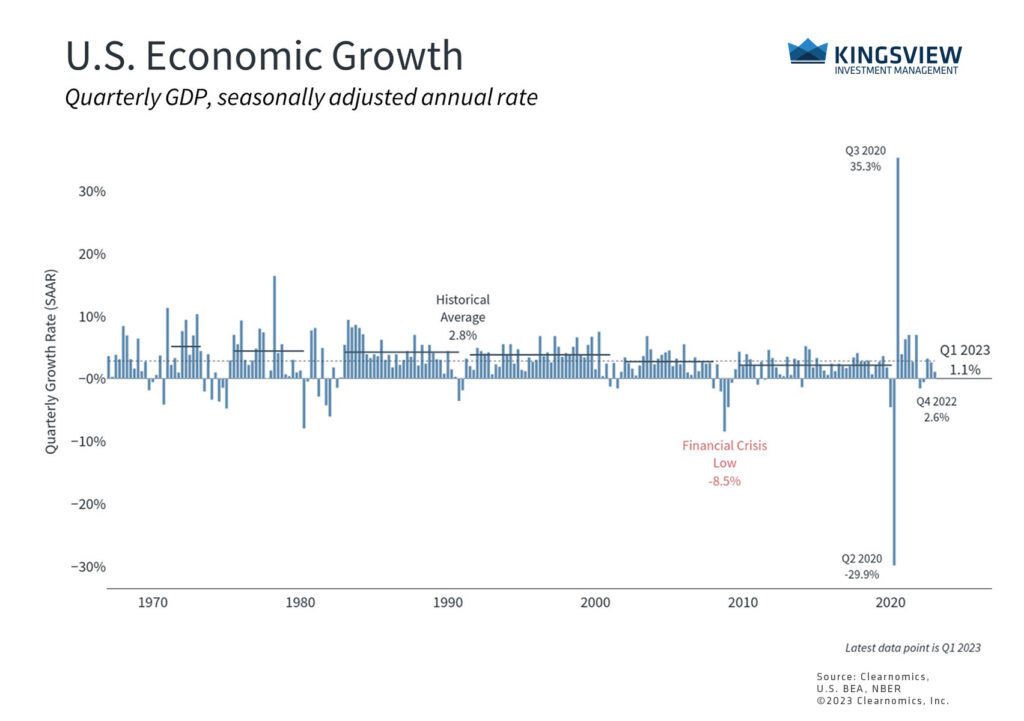

The economy grew at a slower pace in the first quarter

Additionally, interest rates have fallen from their recent peaks which will help shore up bond portfolios. The 5-year Treasury yield, which roughly aligns with the average bond maturity across bank portfolios, has declined from 4% at the end of 2022 to 3.6% today. Ironically, this is in large part because of the banking crisis which was worsened by rising rates. What’s more, the Fed is only expected to raise rates once more this cycle, possibly at its May meeting, before pausing and assessing the situation. This is helped by improving headline inflation numbers.

Finally, the broader economy continues to be stable, even if it does appear to be slowing. Last week’s GDP report showed that the economy grew by 1.1% in the first quarter. This was slower than expected but was primarily due to a decline in inventories among businesses which reduced growth by 2.26 percentage points, a factor that could reverse later this year. Fortunately, this was offset by strong consumption spending which added 2.48 percentage points. Overall, a slowing economy is what the Fed expects to see in a tighter rate environment.

The bottom line? Long-term investors should continue to maintain perspective in light of the ongoing banking crisis. A combination of company-specific factors as well as the broad macroeconomic environment led to challenging conditions for these particular banks. However, parallels to 2008 and other historical episodes are premature. During times of market uncertainty, the best approach is to stay diversified and not overreact to news headlines.

Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. Investment advisory services offered through Kingsview Wealth Management, LLC (“KWM”), an SEC Registered Investment Adviser. (2023)