Portfolio Manager Insights | What the Fed’s Latest Projections Mean for Long-Term Investors — 9.27.23

At its September meeting, the Federal Open Markets Committee kept rates unchanged with a target range of 5.25% to 5.50%, in a decision that was widely anticipated by investors. Still, markets responded negatively with bond yields jumping to levels not seen since 2007, the S&P 500 falling a couple percentage points, and tech stocks retreating further from their recent peaks. This reaction may come as no surprise to investors since disagreements around the direction of the economy and Fed policy have driven market swings all year. In addition, issues such as a possible government shutdown, cracks in China’s economy, student loan payments, higher oil prices, and more, are worrying investors. As we approach the final quarter of the year, how can investors maintain perspective on the state of the economy and its impact on markets?

Markets have rallied this year due to factors such as better-than-expected economic growth, improving inflation, and a more stable financial sector. It’s important to remember that today’s environment is not only far better than most investors had hoped for just a year ago, but exceeds many of the rosiest projections by Wall Street analysts. Despite this, the central question that still divides investors is whether the Fed will make a policy mistake, which in this case could involve keeping rates too high for too long. This is because the Fed has maintained a “hawkish” posture as it combats inflation, utilizing not only higher interest rates, but a shrinking balance sheet and firm forward guidance.

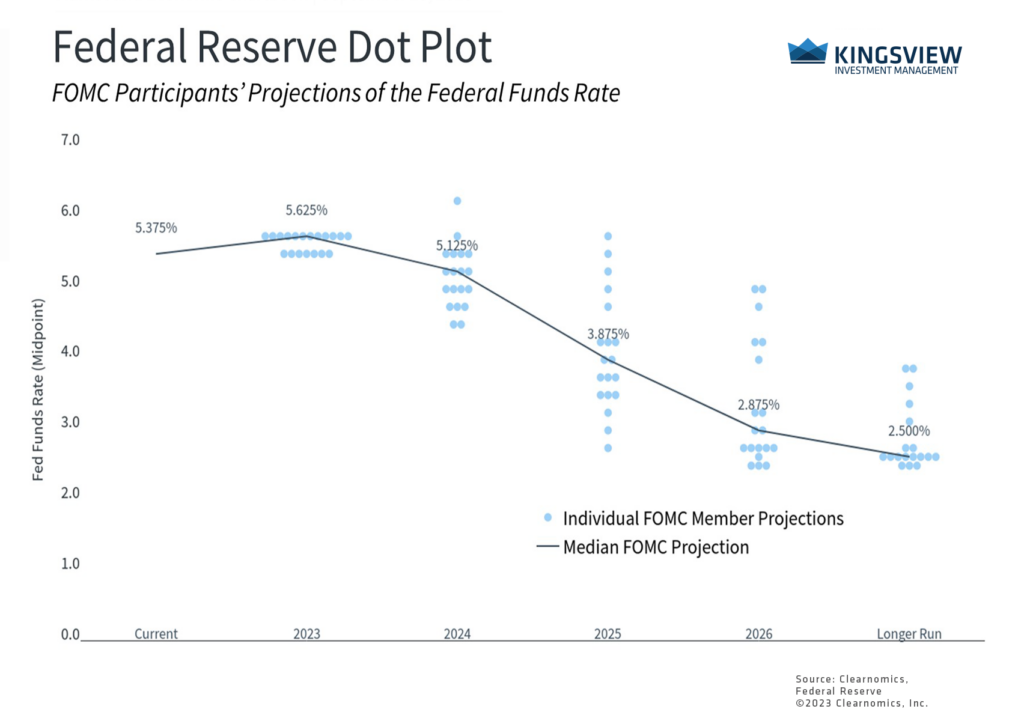

The Fed expects to keep rates higher for longer

The term “forward guidance” refers to the expectations that the Fed sets through its communications. These communications have evolved significantly over the past three decades. During the Greenspan era of the mid-1980s to mid-2000s, Fed decisions were typically made with simple written statements, often only a few short paragraphs. Beginning in 2011 under Ben Bernanke, the Fed began holding quarterly press conferences and publishing its Summary of Economic Projections “to present the Federal Open Market Committee’s current economic projections and to provide additional context for the FOMC’s policy decisions.” During Janet Yellen’s tenure, further changes were made to expand the Fed’s forward guidance and provide more clarity on the expected path of rates.

Today, under Jerome Powell, the Fed Chair now hosts a press conference after every meeting, even when there is no change in the fed funds rate. This is in addition to the numerous other speeches and written pieces by the Fed Chair and other Fed officials. The Fed’s use of forward guidance means that rate decisions are often telegraphed well in advance, resulting in few surprises. Thus, the market’s reaction is often more in response to the press conference and the Summary of Economic Projections.

The Fed’s latest projections show that it expects to raise rates one more time in 2023, with only two meetings to go. While markets are somewhat skeptical, there is a higher probability of this occurring in December based on fed funds futures. The Fed also revised its forecasts to reflect a much stronger economy, with expected GDP growth this year shifting from 1.0% to 2.1%, and the unemployment rate falling from 4.1% to 3.8%. Perhaps most importantly for market expectations, the FOMC’s estimate of future policy rates jumped as well in response to these stronger economic conditions. Rather than the fed funds rate falling to 4.6% and 3.4% by the end of 2024 and 2025, respectively, the committee now believes rates will stay higher at 5.1% and 3.9%.

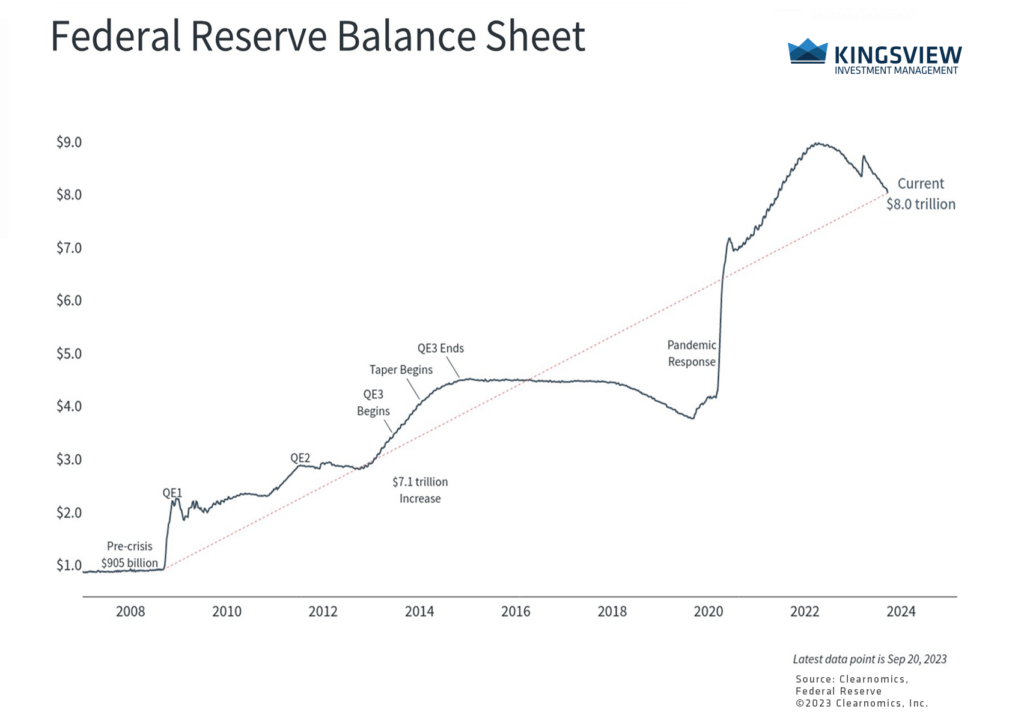

The Fed is also shrinking its balance sheet to tighten conditions

This is one reason that interest rates have jumped with the 10-year Treasury yield rising above 4.5% for the first in 16 years, acting as a drag on both stock and bond prices. Additionally, two other factors complicate the outlooks for policy and inflation, even if they don’t undo the strong improvements of the past year.

First, the Fed is not just raising rates but has also been shrinking its balance sheet, often referred to as “quantitative tightening.” By not maintaining or increasing the size of its balance sheet, the Fed reduces the amount of liquidity in the system. Mechanically, the Fed is bidding on and buying fewer Treasury and mortgage-backed securities, potentially lowering their prices and raising their yields. In effect, this raises rates and tightens financial conditions. Thus, this has the opposite effect of the asset purchases the Fed employed during 2020 and throughout the 2008 financial crisis.

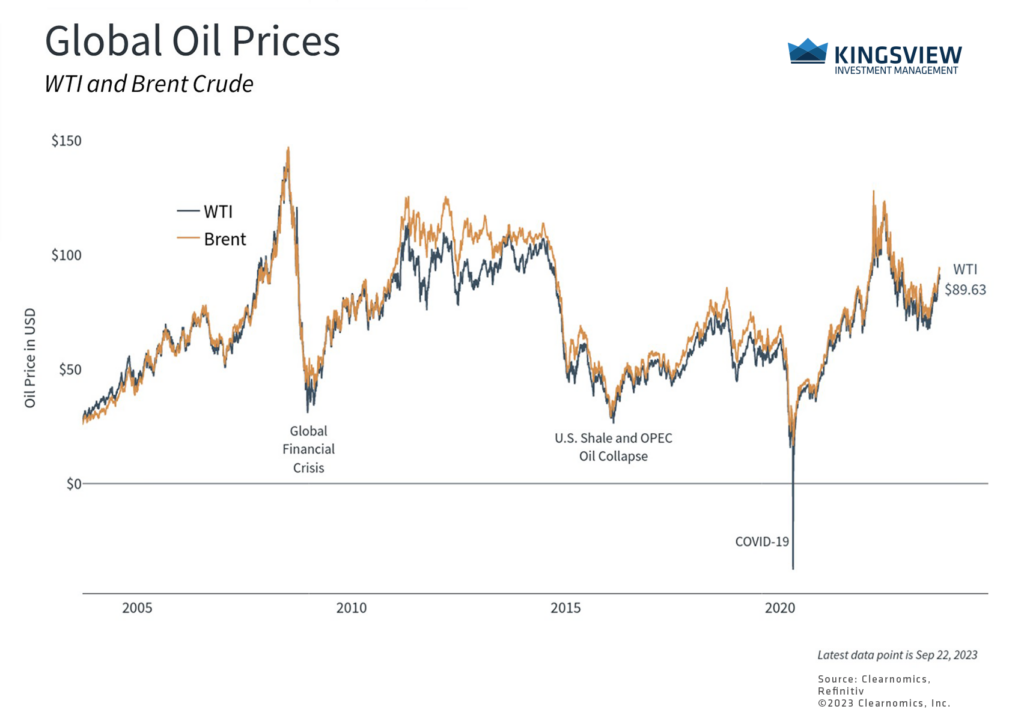

Second, many signs of inflation still persist including higher rent prices, wage growth, and rising oil prices. In particular, oil prices that have jumped back to $90 per barrel and above may be worrisome since this was one of the original catalysts for higher headline inflation in early 2022. Similarly, wage growth around 4.5% year-over-year, while positive for households and consumers, can be problematic from an economic standpoint if this drives prices higher. This is especially true given the historic strength of the labor market.

Oil prices have rebounded in recent months

Of course, investors are worried about many other issues beyond the Fed. This is nothing new – the endless stream of headlines always contains reasons for investors to be fearful of the market. And, although stock and bond prices have pulled back in the third quarter, year-to-date gains are still quite strong by historical standards. This goes to show that it is difficult to predict what the market may do next.

Ultimately, what drives returns for investors are not individual Fed decisions or economic data releases, but the longer-term trends in the economy and markets. In times like these, it’s important to stay disciplined and remember that conditions today are far better than investors could have hoped for a year ago.

The bottom line? The Fed kept rates steady in September but their projections suggest that rates could remain higher for longer. Long-term investors should continue to maintain perspective by focusing on continued economic and market progress, rather than individual data points.

Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. Investment advisory services offered through Kingsview Wealth Management, LLC (“KWM”), an SEC Registered Investment Adviser. (2023)