Portfolio Manager Insights | How Challenges in Commercial Real Estate Impact Investors — 5.17.23

The repercussions of inflation, Fed rate hikes, the ongoing banking crisis, and the approaching debt ceiling deadline are being felt throughout the financial system. One area directly impacted by these shocks is real estate, across both the residential and commercial sectors. Commercial real estate (CRE), in particular, is highly dependent on regional and smaller banks, including those that have struggled or failed since early March. Some investors and economists are concerned about what this might mean for the broader economy in the months to come. What perspective do long-term investors need on real estate in this environment?

Commercial real estate is a broad asset class that includes many types of investments including office space, retail, industrial, and multifamily residential projects. Different factors impact each class of CRE including the pace of economic growth, industrial and manufacturing activity, retail spending, consumer confidence, and more.

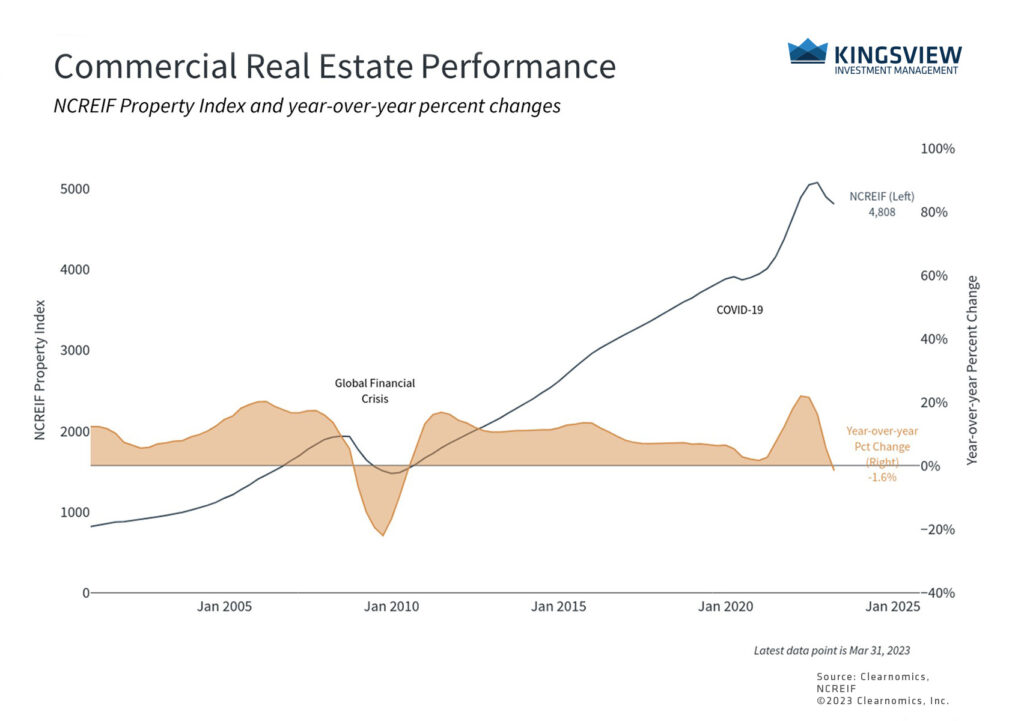

Over the past few years, office vacancy rates have been a primary focus in the news due to the pandemic and the rise of hybrid work models. According to the National Association of Realtors, U.S. office vacancy rates rose from 9.4% prior to the pandemic to 12.5% at the end of 2022, and these rates are undoubtedly worse in many major cities. Overall CRE prices have declined 1.6% over the past year, driven primarily by office space. In contrast, hotel and industrial properties have risen over this period as demand has recovered.

Commercial real estate has struggled the past year

Since CRE projects are often capital-intensive and have heavy financing needs, rising interest rates and instability in the banking sector hurt new projects and existing ones that require refinancing. Due to the size of the CRE loan market and importance of smaller regional banks for CRE credit, the two are tightly linked. Smaller banks are a critical source of credit for CRE capital expenditures and CRE loans are an important source of business for small banks.

According to the recently released Financial Stability Report by the Federal Reserve, smaller banks (those with $100 billion in assets or less) hold more than two-thirds of CRE loans by dollar value, totaling nearly $1.6 trillion. When midsize and regional banks are included, this proportion jumps to 87%. Similarly, the Fed’s latest Senior Loan Officer Opinion Survey suggests that both the demand and credit conditions for CRE and industrial loans have tightened. From a microeconomic perspective, these data show that the CRE industry may continue to face challenging times ahead, and projects will depend heavily on the ability to secure financing and on the quality of banking relationships.

From a macroeconomic perspective, these trends are a symptom of slower growth and higher rates, and not a cause. Thus, it’s not yet clear that these factors will have a large impact on the broader economy beyond what is already occurring. This is because most regional and smaller banks do appear to be healthy despite the ongoing banking crisis. Two months after the collapse of Silicon Valley Bank and weeks after First Republic was purchased by JPMorgan, it’s clear that the banks impacted the most are those that grew too quickly or had concentrated deposits. So, while there may be additional shake-ups in the industry, a repeat of 2008 is far from guaranteed.

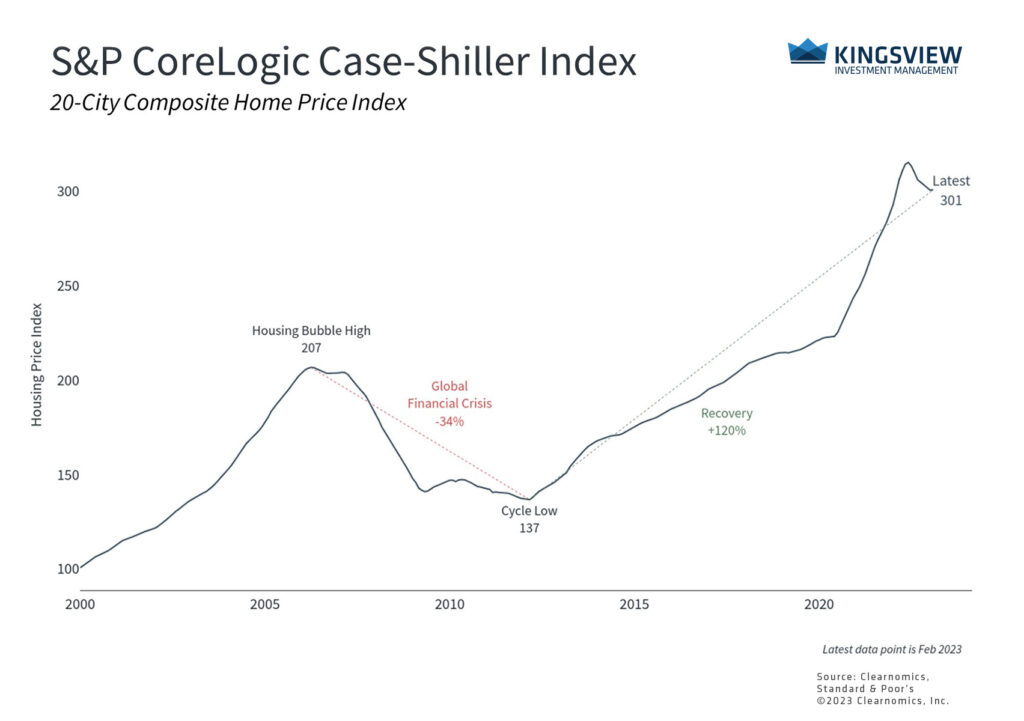

Housing prices have fallen from their recent peaks

Of course, the effect of rising rates has been affecting residential real estate for over a year. The housing market had already experienced an unsustainable run-up during the pandemic as buyers sought more space. Thus, it’s no surprise that both residential housing activity and prices have decelerated as rates have risen and economic growth has stalled.

Specifically, the average rate on a 30-year fixed mortgage currently sits at 6.3% after rising above 7% last November for the first time since 2002. This exceeds the 30-year average of 6% and is well above the average of 4.2% since 2008. Mortgage refinancing activity has plummeted ten-fold and many homeowners are reluctant to give up their locked-in rates. This has led to a sharp deceleration in the Case-Shiller index, a gauge of home prices across the country.

The housing market affects the economy and financial markets in important ways. As individuals, primary residences are usually the most important assets on household balance sheets, and monthly mortgage payments are the largest expenses. As diversified investors, the housing market can represent an income-generating asset class as well as a macro-economic indicator. Rising home prices can bolster financial confidence and spur consumer spending, and vice versa, a fact often referred to as a “wealth effect.”

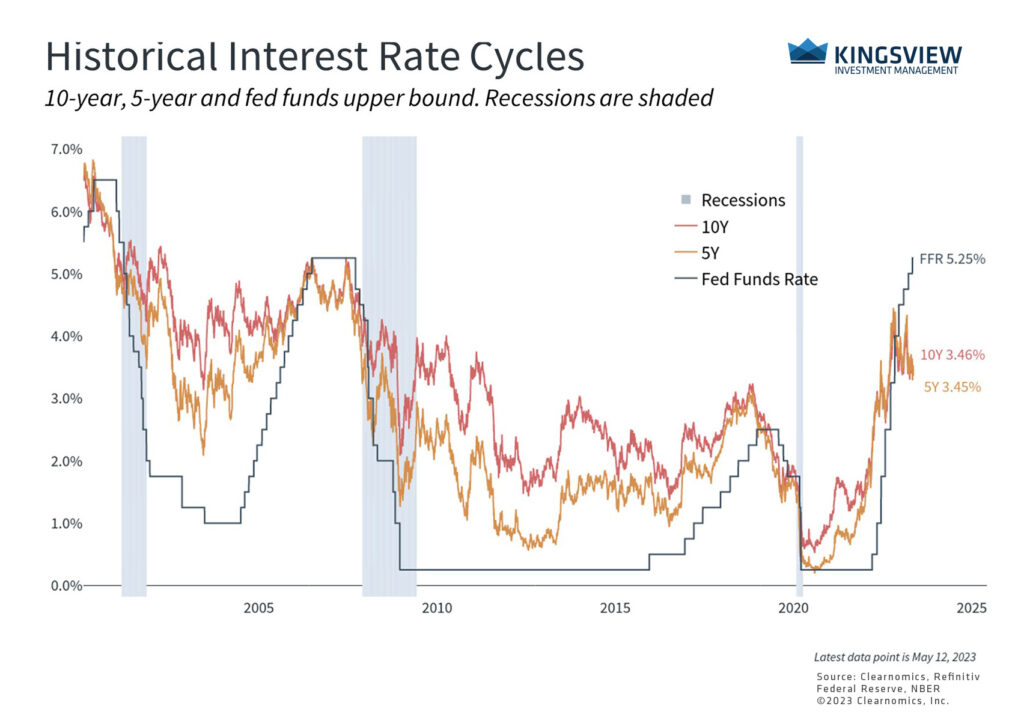

Fed policy rates are far above market rates

Despite these historic challenges across commercial and residential real estate, few investors expect a repeat of the 2008 crisis driven by a bubble in residential housing and significant financial leverage. In this context, it’s important to maintain perspective around the current economic and market environment.

As the accompanying chart shows, the Fed has tightened conditions rapidly to combat inflation, and policy rates are now far above long-term market rates. Thus, it’s not surprising that this would create instability in some parts of the economy, especially in areas that are rate-sensitive such as real estate. After all, the Fed’s goal is to slow economic growth in order to rein in inflation. So, while there may be industry-specific concerns within real estate, and CRE in particular, long-term investors ought to maintain a broader view of the economy to position for the years ahead.

The bottom line? While there are challenges in areas such as commercial real estate, investors ought to stay diversified and balanced in order to navigate this period of financial and economic instability.

Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. Investment advisory services offered through Kingsview Wealth Management, LLC (“KWM”), an SEC Registered Investment Adviser. (2023)