Portfolio Manager Insights | 5 Insights for Navigating Banking Crises in Q2 and Beyond — 4.5.23

In times of market uncertainty, investors often turn to sayings such as “those who fail to learn from history are doomed to repeat it” and “history never repeats itself, but it does often rhyme.” When it comes to the day-to-day headlines, both quotes are relevant given the long history of banking crises and market swings.

This is because investors must deal with innumerable challenges over the course of their financial lives. In just the last few years, portfolios and financial plans have been tested by the pandemic, the highest inflation rates since the 1980s, global conflicts, political uncertainty, asset bubbles, swiftly shifting monetary policy, and much more. Even when times are otherwise calm and markets are steadily rising, including from 2009 to 2020, investors and the media always find reasons to be worried. So, while it’s important to understand the individual issues, it’s perhaps more important to maintain a broader perspective based on the lessons of history.

Of the various challenges investors face today, the banking crisis was perhaps the biggest unforeseen event. It’s now clear that FDIC-insured banks hold bonds that are worth hundreds of billions less due to rising interest rates. Banks such as Silicon Valley Bank and Signature Bank had customers concentrated in specific industries, such as tech and crypto, that made them susceptible to liquidity problems and bank runs. In Europe, Credit Suisse may have had strong capital and liquidity ratios, but ongoing problems made it susceptible to a bank run.

The reality is that the banking crisis will take time to play out. Although modern investors are accustomed to a rapid news cycle, it often takes time for cracks to form, problems to be identified, events to play out, solutions to be implemented, and finally for the system to stabilize.

Many historical examples underscore this. During the global financial crisis for instance, the housing market had already begun to falter by 2006. Bear Stearns failed in March 2008, but the Lehman collapse didn’t occur until September. During the 1998 Asian currency crisis, the first signs of trouble occurred with Thailand in July 1997. The hedge fund Long-Term Capital Management wasn’t bailed out until September the following year. In some ways, the COVID-19 pandemic is the exception given how quickly it reached the U.S. and induced an economic lockdown, but it’s also the case that three years later, we are still experiencing aftershocks.

So, there are always reasons to be on the edge of one’s seat. However, there are reasons for optimism too. The market, economy, and the financial system have been more resilient so far in 2023 than many expected. The job market has been surprisingly strong despite layoffs in tech. Inflation has improved markedly across key areas such as energy and goods. Interest rates rose swiftly early in 2021 and throughout 2022 but have stabilized more recently with the 10-year Treasury yield ending the first quarter at 3.47%. Even the stock market has improved with the S&P 500 having gained 7.6% and 7.5% across the last two quarters.

History shows that markets often turn around when investors least expect it. To put it more strongly, long-term investors are often rewarded precisely because they are willing to accept and manage risk when others are not. Below, we highlight five important insights to guide investors through the coming months.

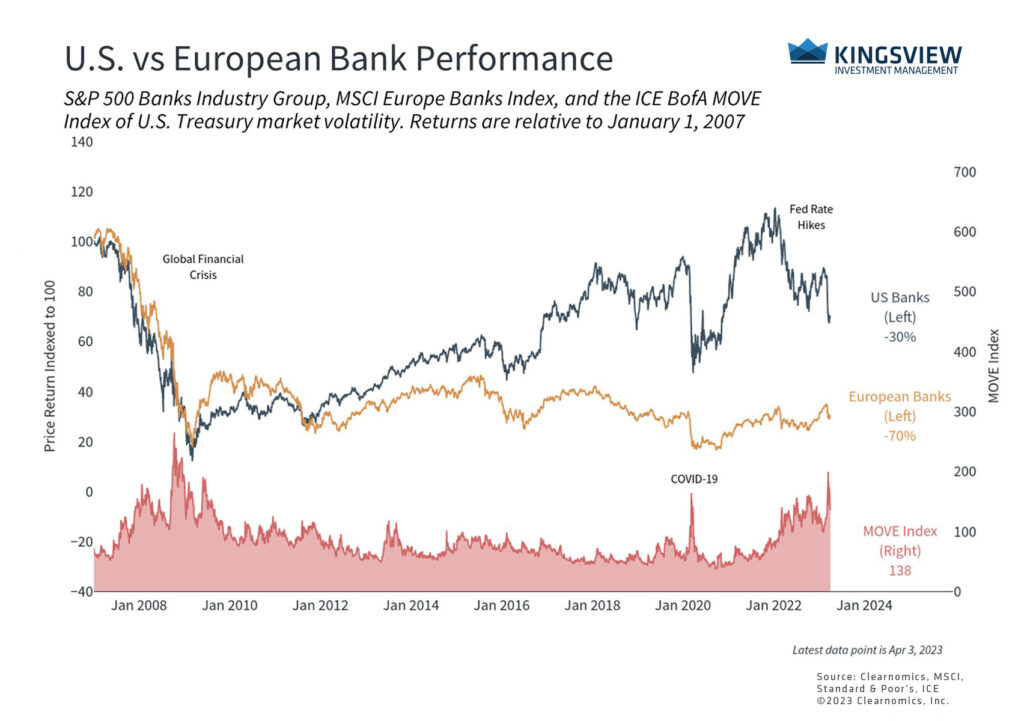

Regional bank stocks have struggled as financial conditions have tightened

It’s no surprise that bank stocks have struggled across markets. In the U.S., this is due to regional banks as the crisis that began with Silicon Valley Bank and Signature Bank plays out. The FDIC, Treasury Department, and the Fed have stepped in to stabilize the system, as have their European counterparts.

The accompanying chart shows the performance of U.S. and European banks. Perhaps most striking, however, is that the MOVE index of bond market volatility jumped to its highest level since the 2008 financial crisis. Fortunately, the situation has stabilized as the initial bank run has calmed. Ironically, this has allowed interest rates to fall which will likely reduce the unrealized bond losses at banks that helped create this situation in the first place.

While there are specific circumstances underlying each of these bank failures, financial instability tends to occur when monetary policy and credit conditions tighten. This is partly because many banks had grown accustomed to high levels of liquidity supporting deposits and their aggressive customer acquisition practices. Thus, it will take time for the banking system to stabilize as the world adjusts to tighter financial conditions.

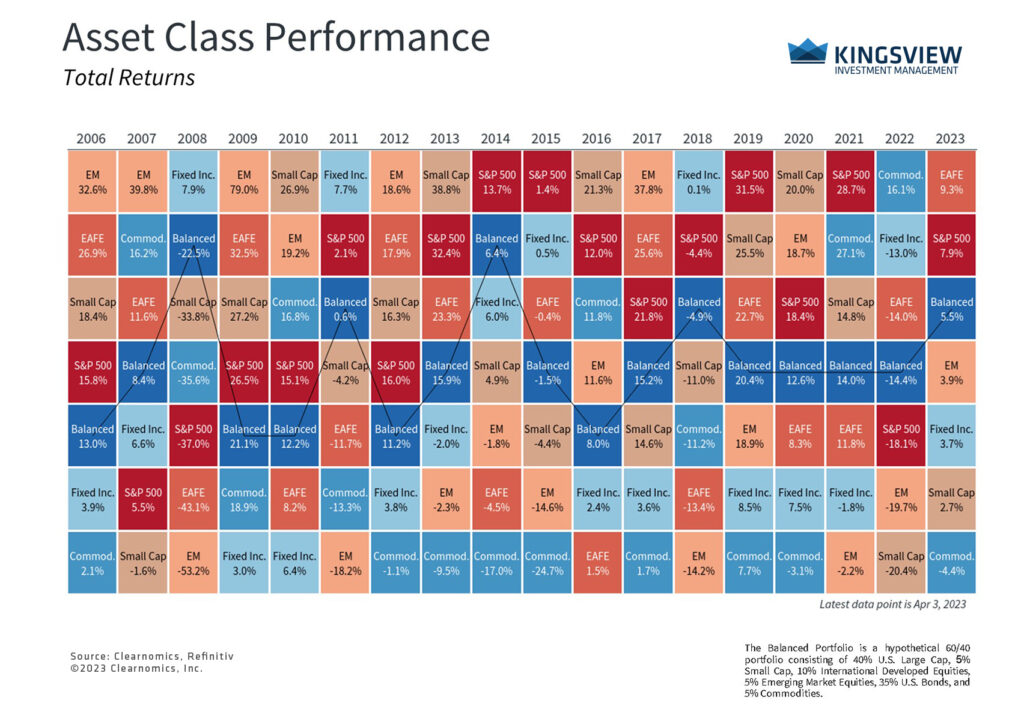

Balanced portfolios have benefited from both stocks and bonds this year

Although only a quarter has passed, markets are already performing much better than last year. This is because interest rates have been more stable and inflation has improved, supporting both stocks and bonds which returned 7.5% and 3.2%, respectively, through the end of the first quarter. A hypothetical 60/40 portfolio generated 5.1% over this same period, underscoring the continued importance of diversification and long-term thinking.

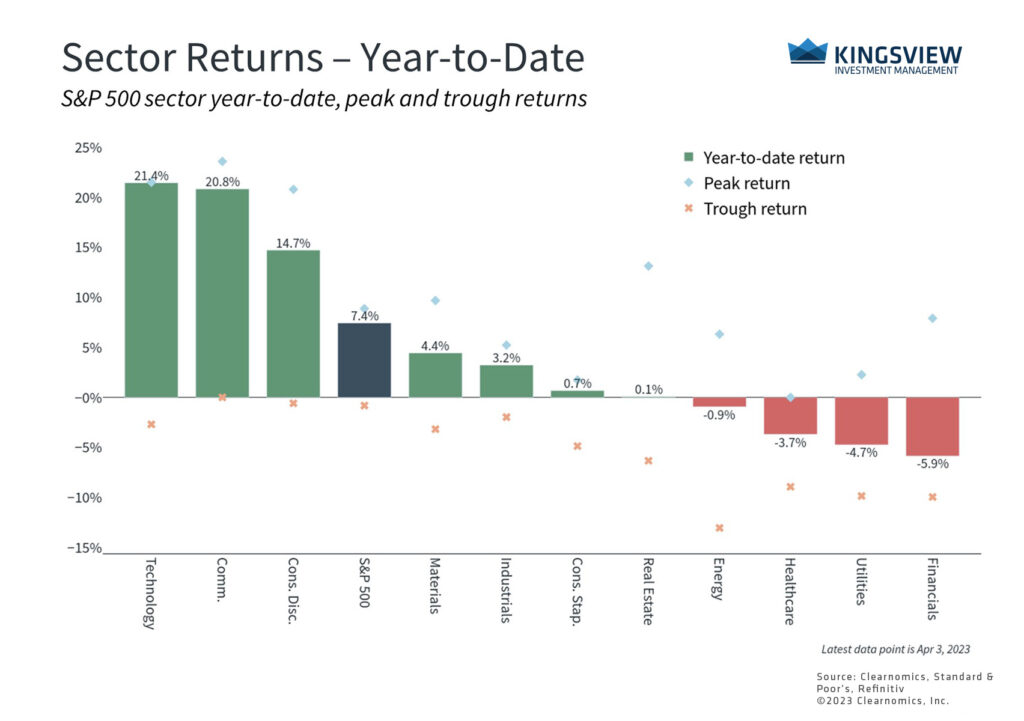

Financials have struggled but tech-related sectors have rebounded

While the S&P 500 Financials sector has struggled due to financial stability concerns, many other sectors have offset it. The Information Technology, Communication Services and Consumer Discretionary sectors have rebounded from last year’s losses as interest rates have fallen and the economy has grown more resiliently than expected. Similarly, the Nasdaq gained 17% with dividends in the first quarter. While investors should not focus too much on only three months of returns, this is a reminder of how quickly market sentiment can shift and of the importance of staying diversified across sectors.

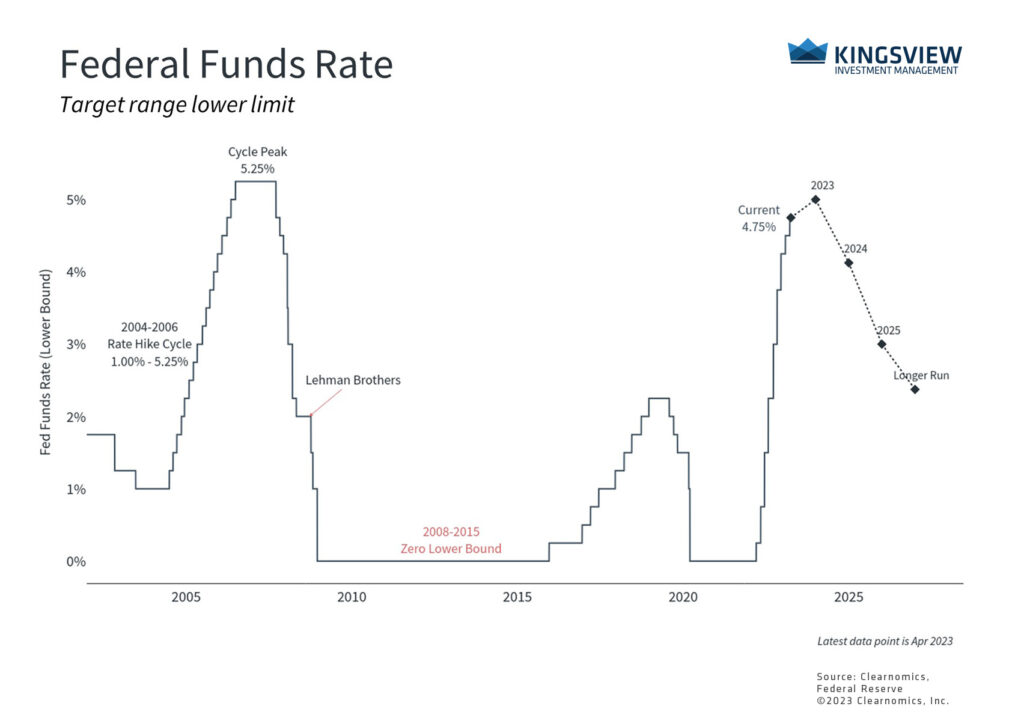

The Fed is expected to slow its pace of rate hikes or to cut rates

The Fed chose to raise rates despite the ongoing banking crisis, in part as a message about their confidence in the financial system. The Fed’s latest projections show that officials expect to keep rates high through the rest of 2023. This is in stark contrast with fed funds futures which show implied rate cuts later this year. Either way, this suggests that the Fed is near the end of its rate hike cycle after one of the sharpest jumps in policy rates in history.

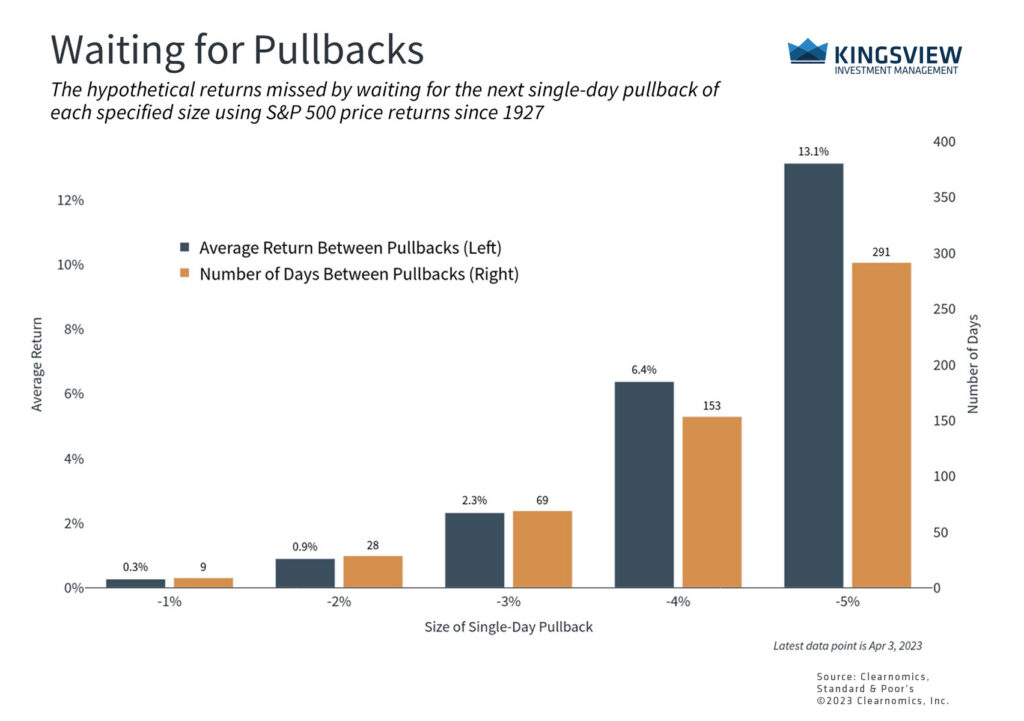

It’s important to stay invested and take advantage of attractive valuations

Ultimately, investors should focus on the long run and not overreact to daily headlines. In particular, valuations are still the most attractive in years as investor sentiment slowly improves. The accompanying chart highlights that staying invested, or taking advantage of better market levels, is often rewarded. History shows that waiting for the next pullback often results in missed opportunities both in terms of returns and the length of time investors need to wait.

The bottom line? While there are ongoing challenges, this is always the case for investors. Staying focused and holding diversified portfolios is still the best way to achieve long-term financial goals.

Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. Investment advisory services offered through Kingsview Wealth Management, LLC (“KWM”), an SEC Registered Investment Adviser. (2023)