Portfolio Manager Insights | 5 Insights for Long-Term Investors in Q4 2023 — 10.4.23

As the final quarter of the year begins, markets are grappling with rising interest rates and continued economic uncertainty. These factors led the S&P 500 to decline 3.3% (with reinvested dividends) during the third quarter while the U.S. Aggregate bond index lost 3.2%. On the surface, these issues echo the many concerns that investors faced last year when inflation and higher rates resulted in a bear market. Other factors including the narrowly averted government shutdown and cracks in China’s economy have also added to investor fears. Amid the seemingly constant stream of negative headlines, how can long-term investors stay positive as they prepare for the final months of the year?

One reason that investing over the course of a lifetime is difficult is the natural tendency to focus on the negative. In psychology, this is often referred to as negativity bias, an effect that causes individuals to allow a few seemingly bad events to outweigh overwhelmingly positive ones. Investors are prone to this cognitive bias because positive news tends to be slow-moving, the result of small gains that compound over time. In contrast, bad news tends to occur suddenly and without notice, resulting in dramatic changes to expectations. Thus, an important discipline for long-term investors is to maintain perspective in order to properly weigh long-term gains against short-term risks.

When it comes to today’s market, focusing only on the negative ignores the many positive developments this year. Specifically, despite some surface similarities to last year, the underlying factors driving markets in 2023 are unique for several reasons.

First, unlike last year when inflation was rising to four-decade highs, inflation is now improving considerably. The Consumer Price Index has decelerated to 3.7% on a year-over-year basis, far below its June 2022 high of 9.1%, while core CPI has slowed to 4.3%. Other measures such as PCE and PPI have shown even greater improvements. This is evidence that the economic shocks from rising prices due to the pandemic supply crunch and spike in consumer demand have already begun to stabilize.

Second, markets declined last year in anticipation of a recession that has not occurred. While a further slowdown is possible, so far the economy has been far more robust than anticipated across many measures. The Atlanta Fed’s GDPNow estimate for the third quarter is still 4.9% and unemployment remains historically low at 3.8%. The economy is doing far better than even the most optimistic forecasts last year predicted.

Third, after one of the most rapid rate hike cycles in history, the Fed is now pausing and waiting. This means that short-term rates are not likely to rise significantly, even if they do remain higher for longer. The initial shocks of rapid policy rate increases have been working their way through the real estate market, the banking sector, technology stocks, and more. As the financial system adjusts to these rates and stabilizes, stock and bond prices could do so as well.

This is not to say that there are not still challenges facing investors in the coming months. Instead, this backdrop is a reminder that while markets tend to rise over long periods of time, they never do so in a straight line. This is true even when the market and economic environment is improving, especially when compared to what investors had expected just a year ago. The following are five key insights to help investors see past the constant negativity in the fourth quarter and beyond.

1. Stocks have held onto strong gains while bonds have struggled

Despite heightened volatility in the third quarter, the S&P 500 has held onto positive gains with the S&P 500 generating a total return of 13.1% year-to-date, with dividends, and the Nasdaq gaining 27.1%. This is in sharp contrast to last year’s bear market and is further evidence that markets can rebound with little notice. The index has been propelled by sectors such as Communication Services (+40.4%), Information Technology (+34.7%), and Consumer Discretionary (+26.7%). Returns in these areas have more than offset poor performances by sectors such as Utilities (-14.4%) and Real Estate (-5.4%).

Unfortunately, higher interest rates mean that the bond market has struggled over the past two months. The U.S. Aggregate bond index has now declined 1% this year, resulting in fears of a repeat of last year. However, not only is this far better than last year’s bond bear market, but bond yields are now at their highest levels in a decade and a half.

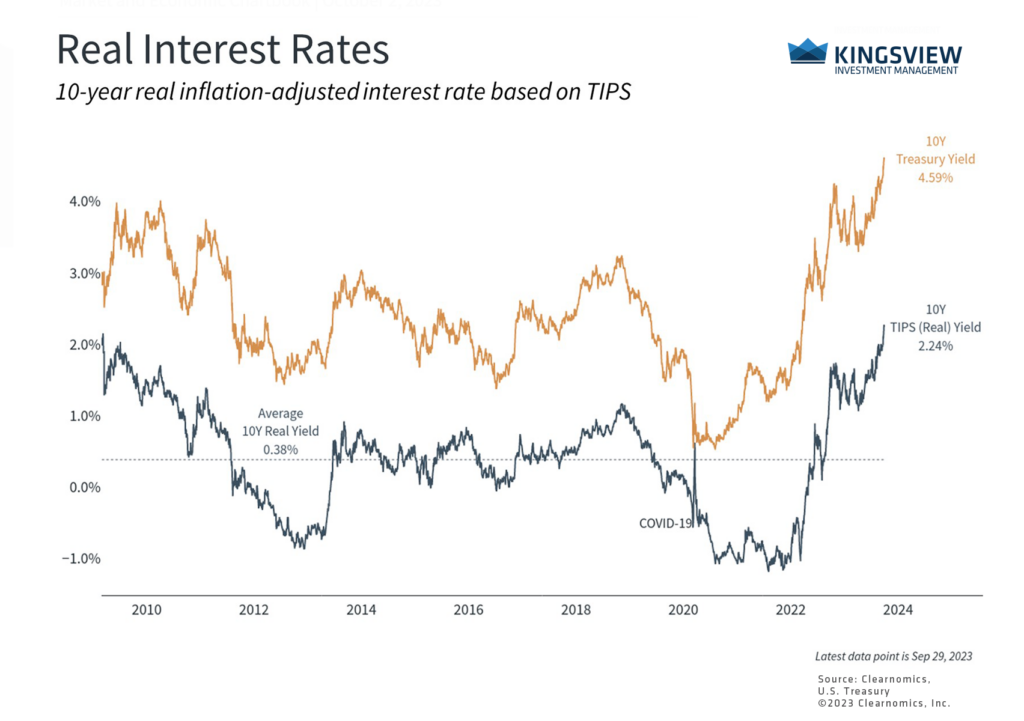

2. Interest rates have risen to 16-year highs

Higher bond yields are positive for investors who can benefit from greater portfolio income. It’s also important to note that these rising bond yields are not the same as last year’s. Improving inflation means that bonds are even more attractive today since “real” interest rates – that is, the value of the interest payments that investors receive after adjusting for inflation – have increased as well. The 10-year TIPS yield is now above 2.2%, resulting in better income generation for investors than at any time since 2008.

Additionally, higher rates this year are a continuation of the uptrend from the past couple of years. In other words, the jump in rates this year is not as much of a surprise to markets as in 2022 when inflation suddenly accelerated. Over time, higher long-term rates could even be a positive if the yield curve re-steepens and economic growth continues.

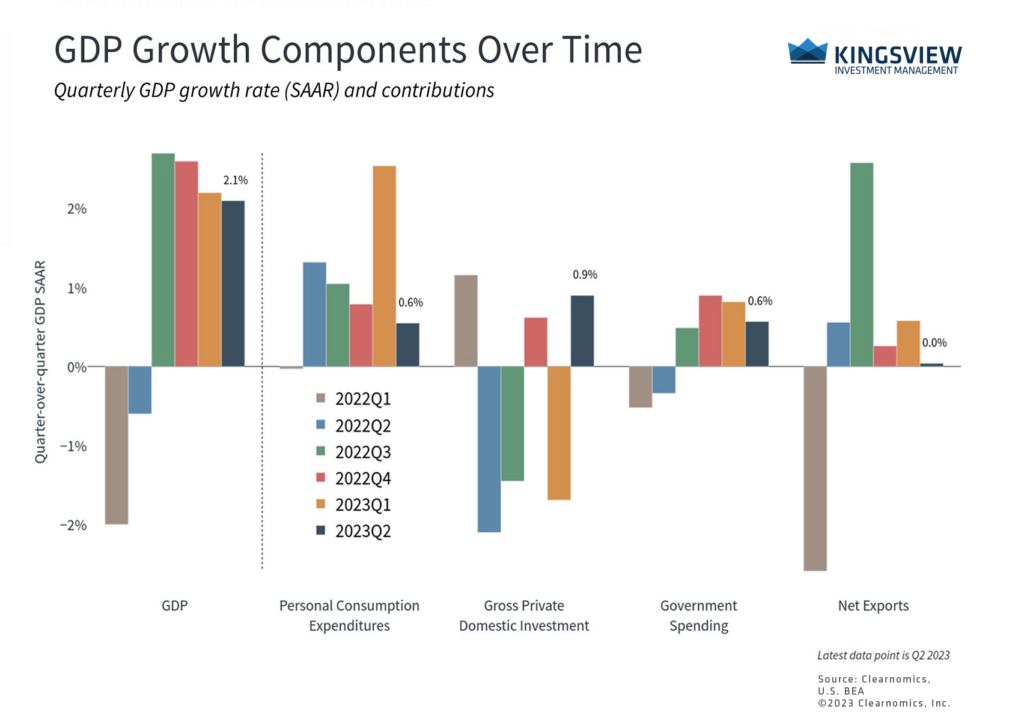

3. The economy has been stronger than expected

Despite the many predictions for a recession in 2023, economic growth has remained robust in 2023. Consumer spending has been stronger than expected while business and government spending have helped along the way. Whether this can continue is an open question, but in the worst case a recession has been postponed to 2024.

On the other hand, the labor market is still one of the strongest in history with unemployment below 4% and wage growth near 4.5%. The number of job openings, while starting to decline, still far outpaces the number of unemployed individuals. Some measures of manufacturing, such as the ISM index, remain in contractionary territory, but the non-manufacturing counterparts have been persistently strong. In all, there are many signs that the economy can continue to grow as the shocks of inflation and interest rates stabilize.

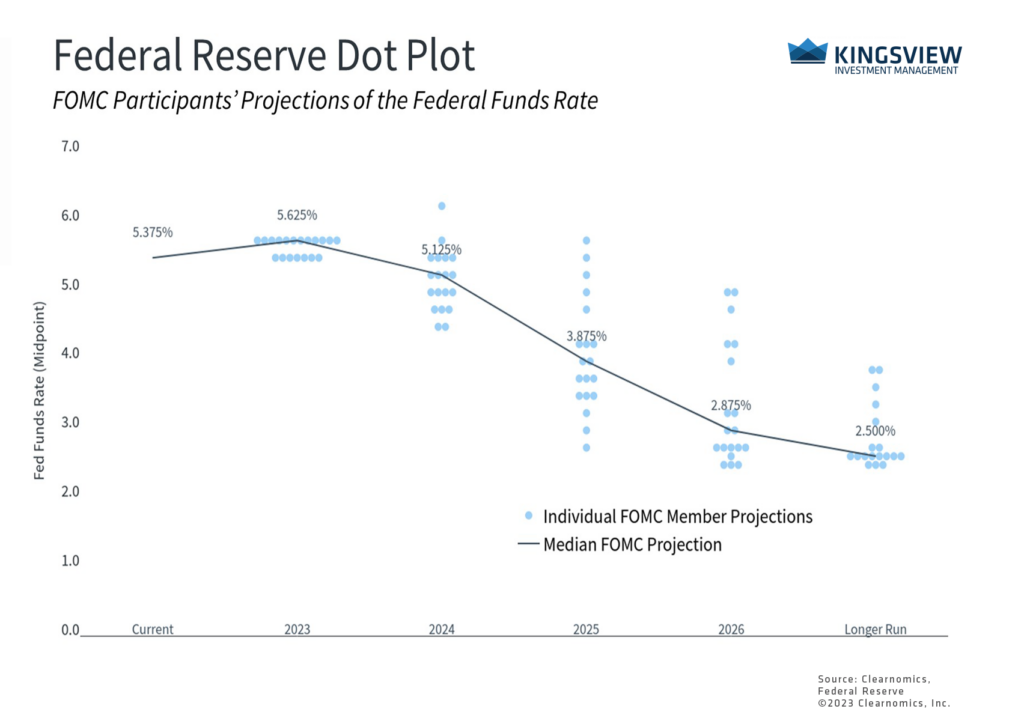

4. The Fed expects to keep rates higher for longer

Improving inflation and stronger-than-expected economic growth have raised the odds of a “soft landing” by the Fed. This has allowed the Fed to slow and pause its rate hikes after a historically rapid pace. This is generally considered to be positive news for markets as the financial system absorbs and adapts to the higher rate environment. While the Fed isn’t expected to lower rates until later in 2024 at the earliest, as shown in the accompanying chart, higher but predictable rates could help support both stocks and bonds.

5. Investors are fully in control of how and when they save and invest

While investment conversations tend to focus on market events, the truth is that investor behavior and activity play as important a role in investment outcomes. This is because saving and investing earlier can have a significant impact due to the benefits of compound interest over time. As the chart above shows, investing just 5 years earlier can result in important differences when an investor reaches retirement. So, while it’s natural to be cautious when markets are seemingly moving sideways and there are negative headlines, history shows that investing earlier – and staying invested – are the best ways to increase the odds of financial success.

The bottom line? Despite the many reasons to be negative, the reality is that the market and economic environment is far better than many expected just a year ago. In the final months of the year, investors should maintain perspective and continue to stick to their financial plans.

Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. Investment advisory services offered through Kingsview Wealth Management, LLC (“KWM”), an SEC Registered Investment Adviser. (2023)