Portfolio Manager Insights | Why Bonds Are Increasingly Attractive for Long-Term Investors — 12.13.23

The bond market has had a better year in 2023 despite ongoing swings in interest rates. The U.S. Aggregate bond index has rebounded 2.7% year-to-date after briefly hovering in the red a few months ago. This is because inflation continues to improve and many investors believe the Fed is not only done raising rates but may begin cutting next year. This is also in stark contrast to 2022 when the bond market fell 13% as interest rates rose swiftly. So, while the bond market is having a better but not exceptional year, the economic climate may be shifting in its favor. What should diversified investors consider as the interest rate story unfolds?

Bond market volatility has remained elevated this year due to the banking crisis and the rate jump that began in late summer. The 10-Year Treasury yield has risen from 3.9% at the start of the year to 4.2% today, briefly hitting 5% along the way. For perspective, the 10-Year yield was only 1.5% at the beginning of 2022 and fell as low as 0.5% in 2020. Both the level and change in rates impact the prices and returns of the bond market, affecting portfolio returns.

Bonds are highly sensitive to interest rate fluctuations

These dynamics have called into question the traditional role of bonds as portfolio stabilizers and consistent sources of yield and returns. Ideally, bonds rise when stocks fall, leading to more balanced portfolios. This was generally the case from the mid-1980s until recently as steadily declining interest rates led to higher bond prices over 40 years. While the past few years have led some investors to question whether this pattern will resume, it’s important to examine why bonds behave this way in the first place.

One way to understand why bond prices tend to fall when interest rates rise is that investors can now buy bonds with higher yields, reducing the value of previously issued bonds. The reverse is also true – when interest rates fall, bond prices tend to rise, all else equal. On a more technical basis, rising rates mean that the present values of future bond payments are worth less than before. This is true when interest rates rise for any reason but can be especially challenging when this is due to inflation.

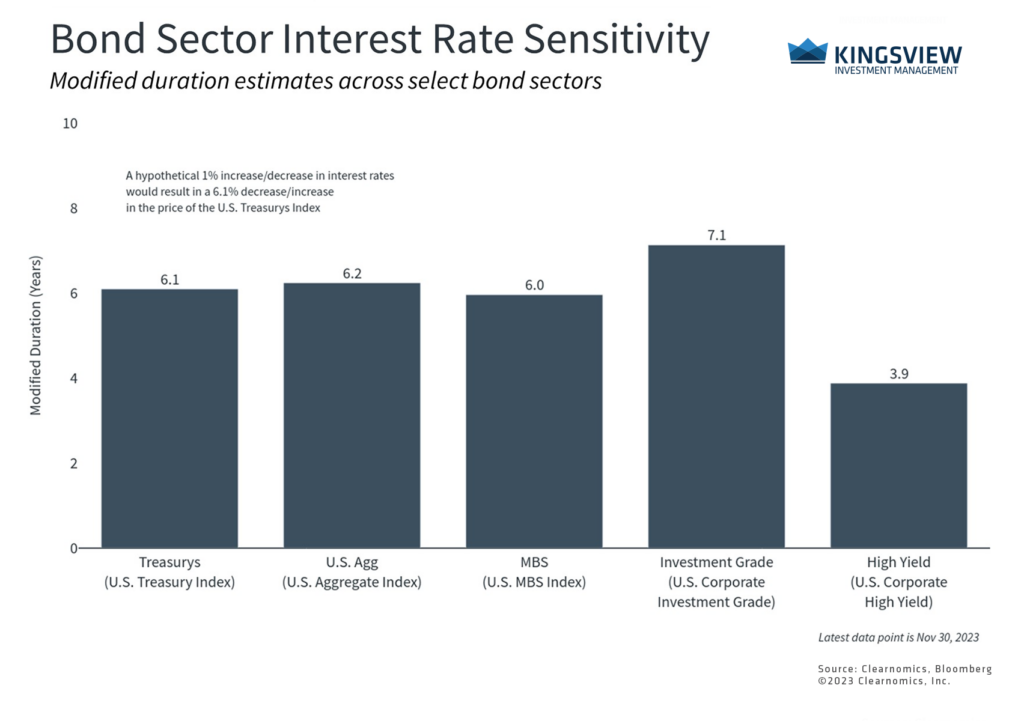

To measure the effect that changing interest rates have on bond prices, investors often use a concept known as “duration” (in this discussion we’ll focus on “modified duration”). In its simplest form, duration tells us how much the price of a bond (or bond index) would gain or lose if interest rates were to fall or rise by one percentage point. For example, the accompanying chart shows that the U.S. Treasury Index has a duration of 6.1 years, implying that a 1% rise in interest rates would result in a 6.1% decrease in the price of the bond index, and vice versa.

Many bond sectors have rebounded in 2023

These calculations are only estimates and make strong assumptions, such as that interest rates rise equally across maturities (which they never do), there is no impact from embedded call options (which is incorrect for certain bonds), and more. Despite being only an approximation, duration is a valuable concept that can help investors understand how bonds perform. For example, the 10-Year Treasury yield rose 2.4% in 2022 which would predict about a 14% decline in Treasury prices – not far off from the realized 13% figure.

Duration varies across bond sectors depending on their characteristics. High yield bonds, for instance, tend to be highly correlated with stocks and have shorter maturities so are less sensitive to interest rates alone. They are among the best performing parts of the market this year as risky assets have surged. High quality corporate bonds, on the other hand, tend to be more sensitive to interest rates since investors buy them for their coupon payments. These bonds have gained 5.2% this year on average as interest rates have stabilized and the economy has grown steadily.

Bond market volatility has been elevated

So, while the jump in interest rates over the past two years has raised questions for some asset allocation strategies, the bond market reaction is easy to understand. These concepts suggest that more stable rates would be a welcome sign for investors and could help to reestablish bonds as portfolio stabilizers. Since duration calculations go in both directions, bond prices could benefit if rates were then to decline. The possibility that the Fed could cut rates next year has already supported bond prices and could continue to do so if long-term interest rates begin to ease as well.

The bottom line? While bonds have struggled as interest rates have risen, there are signs that rates could stabilize in the year ahead. Long-term investors should remain diversified across stocks and bonds as they work toward their financial goals.

Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. Investment advisory services offered through Kingsview Wealth Management, LLC (“KWM”), an SEC Registered Investment Adviser. (2023)