Portfolio Manager Insights | What Washington Politics and the National Debt Mean for Long-Term Investors — 10.18.23

While war escalates in the Middle East, a political battle is also heating up in Washington. As of this writing, there is still no House speaker in Congress after Kevin McCarthy’s exit and Steve Scalise’s withdrawal over the past two weeks. While a number of Republican and House votes are scheduled to attempt to resolve this leadership vacuum, there are more political hurdles on the horizon. This only complicates the market and economic environment for investors who are already navigating higher interest rates, Fed uncertainty, stock market volatility, and more. What can investors do to keep politics in perspective as the situation in Washington evolves?

When it comes to financial planning and investing, it’s always important to separate political views from portfolio decisions. As citizens, voters and taxpayers, expressing political preferences via the ballot box, campaigning and community organizing is an important part of democracy. However, while Washington politics do affect our personal and professional lives, and legislation can impact specific industries and companies, they don’t always impact the stock market the way we might expect. While it may seem unintuitive to some, history shows that markets can perform well in many political environments and leadership configurations across the White House and Congress.

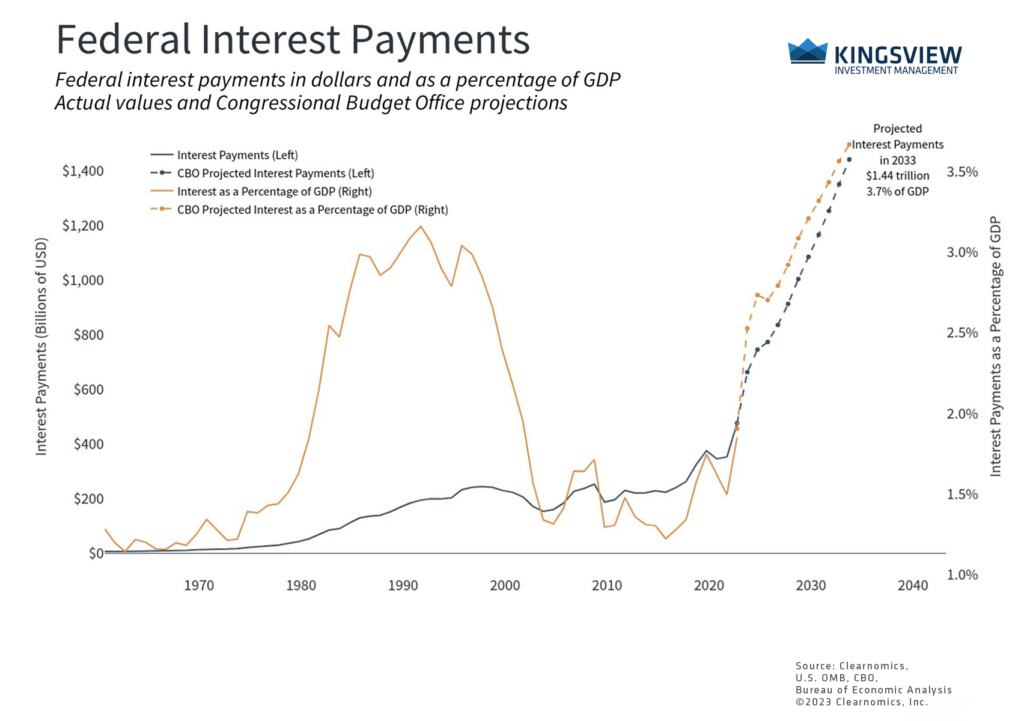

Interest payments on the federal debt are expected to rise past historic peaks

Still, investors should be aware that news headlines over the ongoing battles in Washington will likely increase market uncertainty and heighten concerns for a few reasons. First, the government needs to agree on a new budget soon. Each year, Congress needs to pass a new spending plan to be signed into law by September 30 when the government’s fiscal year ends. This year, Republicans and Democrats were only able to settle on a 45-day funding bill, effectively kicking the can down the road. This means that the clock is ticking and, without leadership and agreement in the House, the odds of hitting a mid-November deadline are less certain.

Perhaps more importantly, a debt ceiling suspension deal was reached earlier this year, but this also only kicked the can down the road to January 2025. While it’s important to establish a budget to maintain government services, not raising the debt ceiling is far worse since the government would be unable to pay its bills, risking a potential government default. While the U.S. has never defaulted on its debt obligations, Washington has increasingly allowed these negotiations to come down to the wire. So, while a default on Treasury securities is still not the most likely scenario, most economists agree that allowing this to happen would have untold effects across all parts of the market and economy.

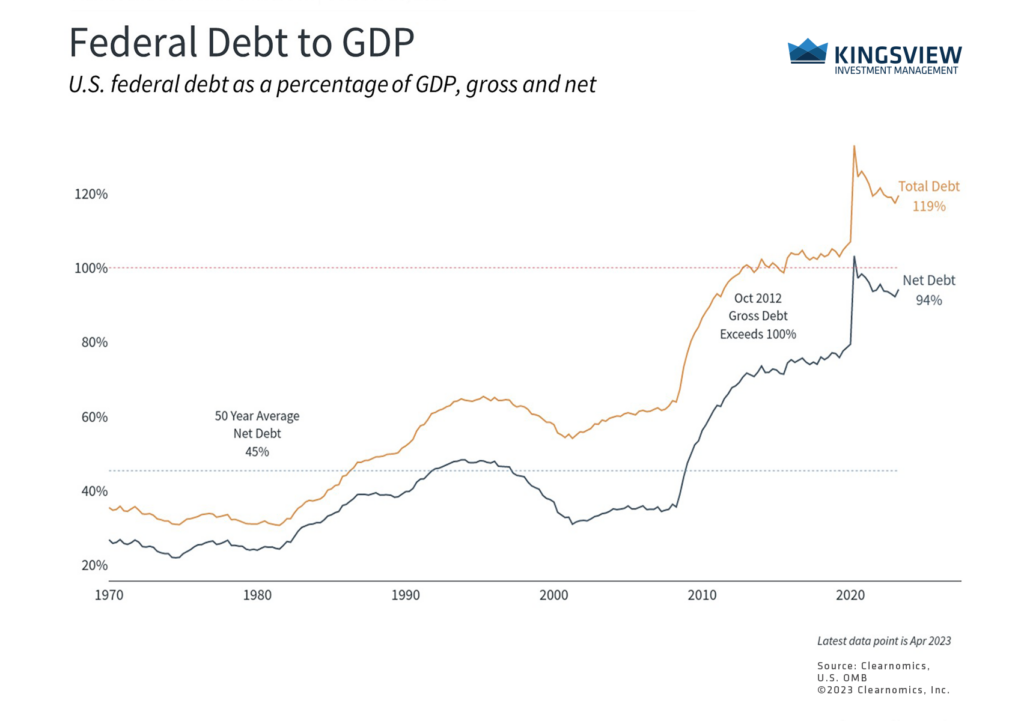

Second, the size of the national debt is a significant concern not just among investors but for everyday citizens. The debt is now greater than the previous debt ceiling level of $31.4 trillion, or 119% of GDP. Unfortunately, this is a complex topic with no easy answers that involves political preferences over spending and taxation, the size of entitlement programs such as Social Security, Medicare and Medicaid, emergency spending programs such as those put in place during the pandemic, and more. One nuance is that a more accurate measure of the size of the national debt is to exclude what the government owes itself. Even this measure, referred to as “net debt” has reached 94% of GDP.

The size of the federal debt continues to worry many investors

Perhaps the more tangible concern for many is not just the size of the national debt but the rising level of interest payments. This is not just due to accumulated debts but is a result of interest rates rising to levels not seen since 2007. The first chart above shows that the dollar amount of interest payments has increased in recent years to $476 billion in 2022, the highest in history. As a percentage of GDP, interest payments are still lower than in the 1980s and 1990s when interest rates were much higher. However, this chart also highlights the Congressional Budget Office’s independent and nonpartisan research which shows that these interest payments could balloon above $1.4 trillion, or 3.7% of GDP, in ten years.

Unfortunately, there are no simple solutions to this issue, especially because fiscal discipline has not been a priority in Washington for some time. That said, prior projections for the national debt and interest payments have not always been accurate, especially in periods when the economy experienced strong growth. Despite the growing debt level, the stock market has also performed well throughout many of these periods. With the benefit of hindsight, making portfolio decisions in response to news on the national debt would have caused investors to miss the entire bull market beginning in 2009, the strong rally in mid-2020, and more.

The market can perform regardless of Washington leadership

Finally, the 2024 presidential race will also heat up in the coming months. Again, while elections matter as citizens, voters and taxpayers, the investment story is different. As the chart above shows, the stock market and economy have grown under all types of leadership in the White House and Congress. There may be occasional short-term hiccups but trying to “time the market” around such events often causes more harm than good. And while there may be historical differences in market performance, the average year is significantly positive regardless of the types of leadership combinations across political parties. There were also many other factors impacting each year’s performance that had little to do with politics.

The bottom line? There are many ways in which politics matter but investors should maintain perspective when it comes to their investment decisions. It will be more important than ever to not be distracted by Washington headlines in the months to come.

Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. Investment advisory services offered through Kingsview Wealth Management, LLC (“KWM”), an SEC Registered Investment Adviser. (2023)