Portfolio Manager Insights | How the Highest Real Yields Since 2009 Affect Investors — 9.6.23

Interest rates have swung wildly over the past two years in response to inflation, economic concerns, and market volatility. After falling as low as 3.3% earlier this year, the 10-year U.S. Treasury is now yielding around 4.2%, back to where it was roughly a year ago. However, while today’s long-term yields look similar to last year’s on paper, they are quite different from an economic and market perspective. What are interest rates telling us today and how does this impact long-term investors?

An important concept in economics is the distinction between “nominal” and “real” values. The simplest way to understand the difference is that nominal values include the effects of inflation while real ones do not. In this way, the labeled prices of goods and services we see every day are nominal prices. For instance, the price of a gallon of milk at the grocery store is a nominal price since it changes based on inflation. The paychecks we receive are also nominal values since they are paid in dollars or other currencies whose purchasing power changes as the prices of goods and services fluctuate.

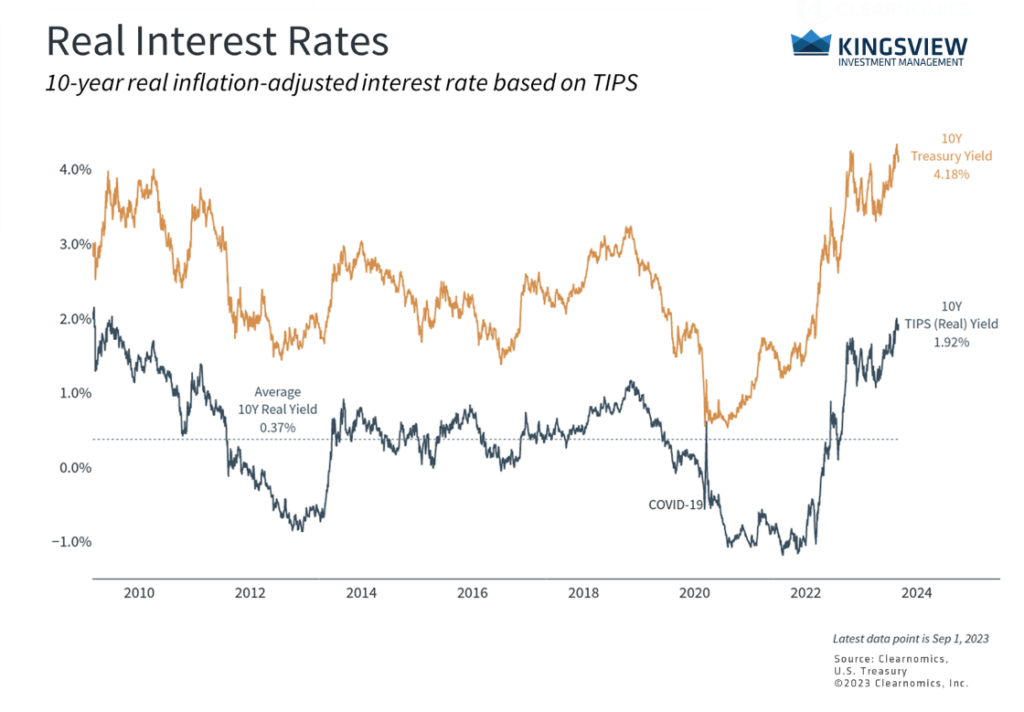

Real long-term Treasury yields are at 14-year highs

A real value, on the other hand, represents the actual amount of goods and services one receives, irrespective of the prices of those items. A gallon of milk, for instance, is still a gallon of milk whether it costs $3.97, as it does today on average across the country, or $2.84 as it did five years ago. If someone were to receive their paycheck not in a set amount of nominal dollars but in the real dollar equivalent of gallons of milk, i.e. an amount that allows them to buy a set number of gallons, they would receive more dollars today. In this way, their paycheck would be protected from inflation, at least in terms of milk.

Why does this matter? When prices are fluctuating, such as in times of high inflation, it’s helpful to understand what we’re actually getting for those prices. For example, getting an annual raise of 4.5% is great, but if inflation is rising at a faster pace, the value of those wages is declining in real terms. The same is true for the purchasing power of cash and anything else that is measured in nominal terms. This is also why economic growth is often measured in terms of “real GDP” since this focuses on the actual output of the economy rather than price movements.

The distinction between nominal and real values is important for investing as well. For example, the 4.2% yield on 10-year Treasury securities mentioned above is a nominal yield. When inflation rises faster than expected, the actual purchasing power of the interest payments an investor receives will be lower, and vice versa. Thus, the real yield one receives depends on the level of inflation and, in some sense, this what should matter to long-term investors. Similarly, investing in stocks has been historically attractive because stock market returns have far outpaced inflation, resulting in positive real returns.

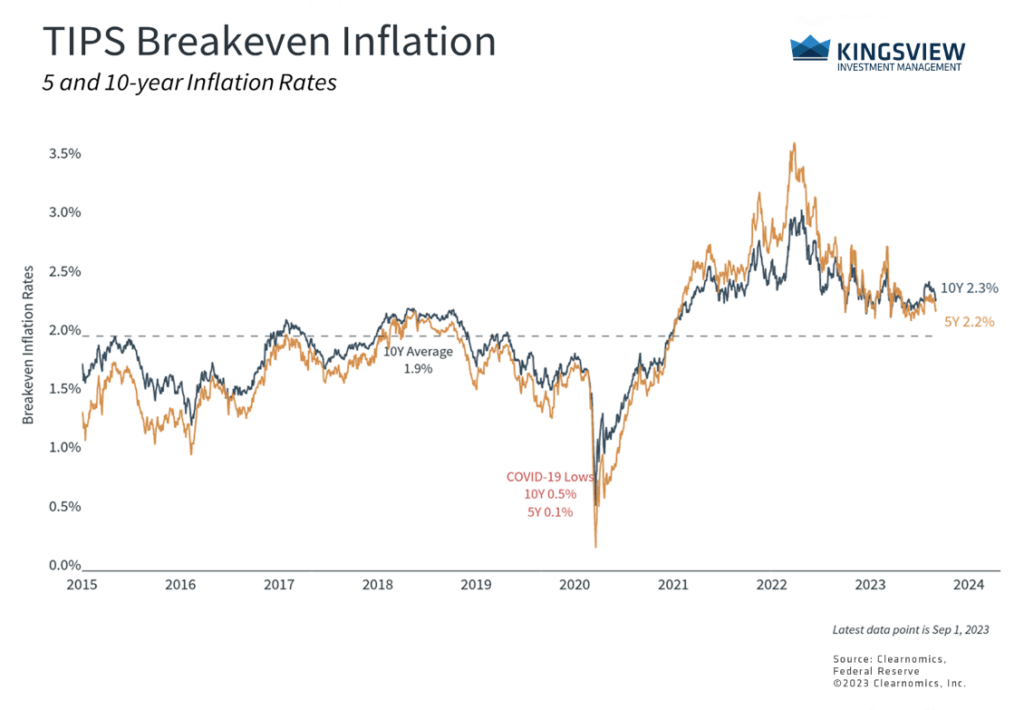

The expected inflation rates implied by TIPS have declined

Fortunately, even though the nominal yield on the 10-year U.S. Treasury appears to be the same as it was last year, the real yield is now at its highest level since 2009. This is because inflation expectations have improved dramatically, as shown in the accompanying charts, and economic growth has surprised to the upside. What’s more, the current real yield of 1.9% is far above the average since the global financial crisis of 0.37% when both nominal interest rates and inflation were low. This is another reason that bonds continue to be attractive and important components of diversified portfolios despite the significant volatility of the past two years.

It’s also important to note that there are bond instruments whose purpose is to generate real yields for investors. Treasury Inflation-Protected Securities (TIPS), for instance, adjust their nominal yields for inflation, thus providing a “guaranteed” real yield. This is similar to the example above where someone chooses to be paid in the real dollar equivalent of gallons of milk – regardless of how the price of milk changes, the real value stays the same. In general, the value of TIPS is the highest when inflation is high and rising, or when investors value the certainty of a specified real yield.

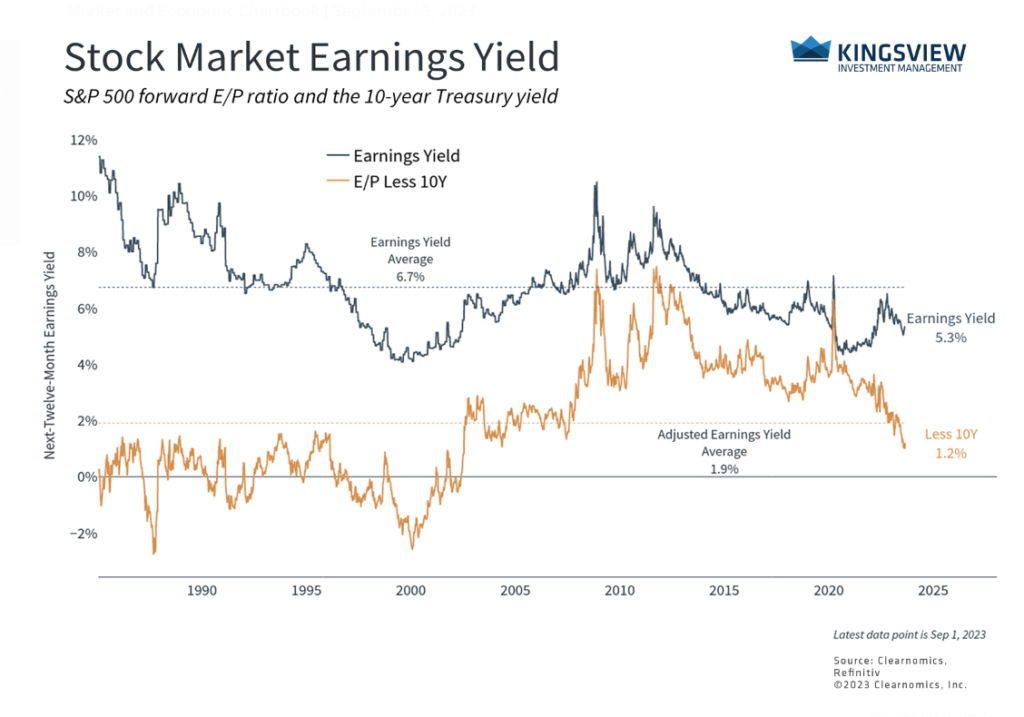

These concepts affect stock market valuations as well. When real yields on bonds are higher, investors may find it more attractive to invest in bonds than riskier stocks, at least on the margin. In other words, the bar for stocks is higher when investors can generate attractive real yields from bonds. Thus, there can be an inverse relationship between higher real rates and stock market valuations in the long run. In the short run, other factors can be more important such as the rally in tech this year. At the moment, the S&P 500 earnings yield of 5.3% is below its historical average of 6.7%, and is even lower when adjusted for the level of either real or nominal interest rates.

Stocks are more expensive relative to bonds as rates rise

Of course, this does not mean that the stock market is not attractive for other reasons or that investors should only hold bonds. As always, long-term investing is about building diversified portfolios that contain the proper allocations of stocks, bonds, and other asset classes depending on financial goals. The fact that real yields are at their highest level in 14 years is one factor for investors to consider as they structure their investment portfolios to increase the odds of financial success.

The bottom line? Investors should understand the difference between nominal and real rates as the economic and market outlook shifts. Real yields have jumped as inflation expectations have improved, providing a source of real income for portfolios.